Yi Gang's latest article, approaching the 7.16 checkpoint and launching a counterattack! Offshore RMB skyrocketed by nearly 500 points | Exchange rate | Yi Gang

RMB counterattack!

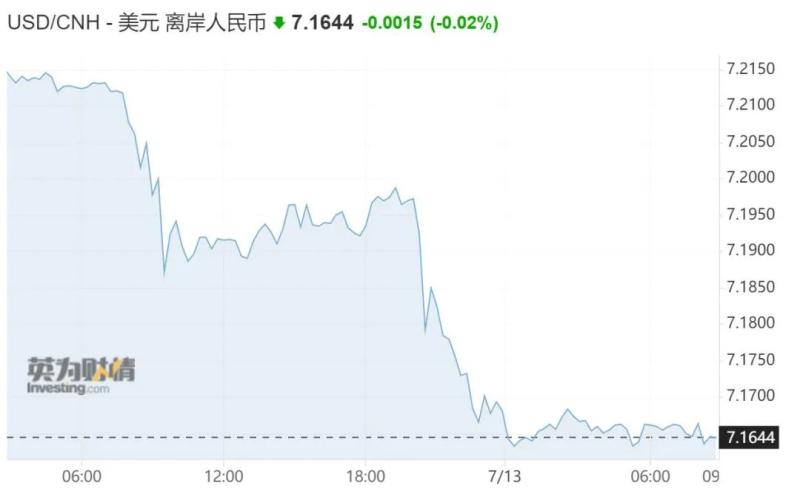

The offshore RMB/USD was at 7.1657 yuan at 04:59 Beijing time, up 462 points from late Tuesday in New York. The overall trading during the day was in the range of 7.2155 to 7.1617 yuan. As of publication, the offshore RMB has been temporarily reported at 7.1644.

The onshore RMB/USD closed at 7.1650 at 03:00 Beijing time, up 445 points from the closing of the previous trading day. The transaction volume is 42.18 billion US dollars.

According to Wind data, the US dollar index has been continuously declining since July, with a significant drop of 1.06% on the 12th. At the same time, the onshore and offshore RMB have rebounded against the US dollar, with both onshore and offshore RMB recovering from the 7.2 level. Since last Thursday, the Chinese yuan has continued to rise against the US dollar. As of yesterday's close, the offshore Chinese yuan has accumulated a total increase of 950 basis points against the US dollar in five trading days.

The Governor of the People's Bank of China, Yi Gang, recently published an article in Economic Research titled "The Autonomy, Effectiveness, and Economic and Financial Stability of Monetary Policy", providing a framework description of China's monetary policy regulation and explaining its basic logic and operational mechanism.

Yi Gang pointed out in the article that interest rate and exchange rate policies must first follow the laws of market economy, which is the key to maintaining stable economic and financial operations and suppressing systemic financial risks from a macro level. The two types of policies are not in a parallel relationship. Interest rates are the core and framework of monetary policy, and exchange rates are formed by the market under the influence of interest rate policies. Monetary policy regulation should first prioritize domestic goals and choose optimal policies such as interest rates to achieve domestic goals. Secondly, it is necessary to create a favorable environment for exchange rates to be determined by the market.

Yi Gang also stated that following the above train of thought, in the context of significant changes in interest rates in major developed economies around the world in recent years, China's monetary policy has not simply followed suit, but has adhered to the principle of "self centeredness", with a significant increase in autonomy and effectiveness. In regulation, complex factors such as time delay should be fully considered. While doing a good job of countercyclical regulation, attention should be paid to cross cycle regulation and cross regional balance. Both tightening and loosening directions should be relatively cautious and leave room for improvement. Monetary policy should always operate within the normal range, and real interest rates should roughly match potential economic growth rates. In recent years, the elasticity of the RMB exchange rate has significantly increased, enhancing the autonomy of interest rate regulation and promoting macroeconomic stability. The stability of economic fundamentals also supports exchange rate stability, making the operation of the foreign exchange market more resilient, and forming a positive interaction between interest rates and exchange rates.

Yi Gang stated that the next step is to do the following work well:

One is to maintain a moderate total amount, adhere to the implementation of a prudent monetary policy, and ensure that monetary conditions match the requirements of potential economic growth and basic price stability. Do a good job in countercyclical and cross cyclical regulation, balance short-term and long-term, economic growth and price stability, internal and external equilibrium, grasp the strength and rhythm of monetary policy regulation, adhere to not engaging in "flood irrigation" and not exceeding the issuance of currency, and provide stronger and higher quality support for the real economy.

"In the future, China's potential economic growth rate is expected to remain within a reasonable range. If conditions permit, we will try to maintain a normal monetary policy, maintain positive interest rates, and maintain a normal, upward slope yield curve shape. We will leverage the role of structural monetary policy tools and increase financial support for key areas and weak links of the national economy." Yi Gang said.

The second is to deepen reform, continuously promote the marketization of interest rates and exchange rates, and prioritize internal and external balance. Continue to improve the market-oriented interest rate formation, regulation, and transmission mechanism, improve the central bank policy interest rate and interest rate corridor mechanism, stabilize market expectations, and promote the reduction of comprehensive financing costs for enterprises.

Steadily deepening the market-oriented reform of the exchange rate, adhering to the improvement of a floating exchange rate system based on market supply and demand, with reference to a basket of currencies for adjustment and management, enhancing the flexibility of the RMB exchange rate, strengthening expectation management, adhering to bottom line thinking, doing a good job in monitoring and analyzing cross-border capital flows and risk prevention, maintaining the basic stability of the RMB exchange rate at a reasonable and balanced level, and better playing the role of the exchange rate as a macroeconomic and international balance of payments automatic stabilizer.

The third is to strengthen policy coordination, continuously improve the macro prudential policy framework, and prevent and resolve financial risks.