What's the solution?, Land transactions have become a major disaster area, and audits have exposed the old problem of local inflated fiscal revenue. Finance | Local

The phenomenon of artificially increasing local fiscal revenue seems to be on the rise.

Recently, some provinces have disclosed audit reports on the execution of provincial budgets and other fiscal revenues and expenditures for the year 2022. Among them, the Hunan audit report found in the special audit of the financial final accounts of 7 counties that 7 counties inflated their fiscal revenue through methods such as land self sale and self purchase; The audit report of Hebei Province found that some cities and counties have inflated their fiscal revenue by buying and selling non operating state-owned assets through a fiscal revenue and expenditure cycle.

At the end of June, the Audit Office released the "Audit Work Report on the Implementation of the Central Budget and Other Fiscal Revenue and Expenditure for 2022", which showed that when focusing on auditing the management of fiscal revenue and expenditure in 54 regions and extending common issues to other regions, one of the problems found was that 70 regions artificially increased fiscal revenue by 86.13 billion yuan through methods such as "selling and buying" state-owned assets and fictitious land transactions, of which 67.5% occurred at the county level.

Several financial and tax experts have told First Financial that inflating fiscal revenue to cover up the authenticity of income is an illegal and irregular behavior, which not only affects the actual available financial resources of local governments, damages government integrity, but also misleads higher-level government decision-making and macroeconomic regulation. In addition to pursuing political achievements and creating false prosperity in regional economy, some places have also resorted to short-term fundraising to alleviate liquidity crises due to local financial difficulties and difficulties in balancing income and expenditure in recent years. In the future, while strengthening supervision, it is also necessary to promote reforms in the financial and tax system to address this issue.

Why inflate fiscal revenue

The inflated fiscal revenue in local areas is an old problem. For example, in 2017 and early 2018, Liaoning and Inner Mongolia self exposed large-scale fiscal revenue fraud, squeezing out the "water" of fiscal revenue and significantly reducing revenue, which attracted external attention. In recent years, the National Audit Office and local audit departments have also repeatedly disclosed the situation of inflated fiscal revenue in some areas.

From the perspective of inflating fiscal revenue, it mainly includes idle operations, fictitious taxable matters, and paying before returning. The so-called idle operation refers to the financial department first allocating fiscal funds in the form of expenditures to payment units or fiscal revenue collection units, and then collecting and storing the fiscal appropriations received by these units again under various names such as taxes and administrative fees. This repeated cycle leads to a virtual increase in fiscal revenue.

However, it is not difficult to find from the above audit reports that it is common to inflate fiscal revenue through false land transactions by state-owned enterprises.

Professor Shi Wenwen from China University of Political Science and Law analyzed that there are many ways for local governments to artificially increase fiscal revenue. However, considering controllable risks, fast and convenient operation, most of them choose state-owned enterprises controlled by the government to operate, such as fictitious land transactions with some government financing platform companies to artificially increase revenue.

In recent years, due to the deep adjustment of the real estate market and the tight funding of real estate developers, the land transfer revenue that many places heavily rely on has significantly declined. In order to support the land market, some places require local government investment and financing platform companies to purchase land, which directly led to a significant increase in the proportion of urban investment and land acquisition last year.

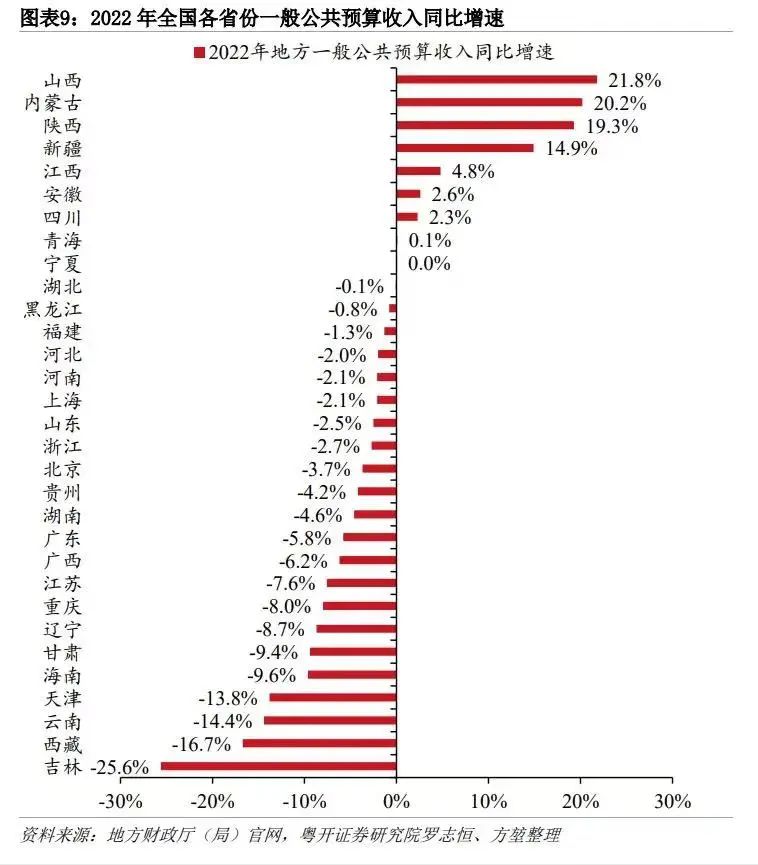

The chart is from Yuekai Securities Research Institute

Although the acquisition of land by urban investment does not necessarily mean a false increase in fiscal revenue, this trend has attracted the attention of the Ministry of Finance.

In the notice issued by the Ministry of Finance in October last year on strengthening the management of "three public" funds and strictly controlling general expenditures, a major point was to require local governments to prevent inflated fiscal revenue. It is not allowed to artificially increase land transfer revenue through state-owned enterprise land purchase or other means, and it is not allowed to falsely increase fiscal revenue by creating false names to fill the gap in fiscal revenue.

A local finance official told First Financial that the main motivation for local government to inflate fiscal revenue is still for political performance, and they want to make indicators such as fiscal revenue growth look good. Because in the end, inflating fiscal revenue does not actually increase financial resources and does not make a significant contribution to local finance.

Wang Zhenyu, Dean of the Institute of Local Finance at Liaoning University, told First Financial that various forms of "virtual increase" in local finance have always existed, but it is different from the "virtual increase" in some provinces more than a decade ago due to unreasonable performance views. In recent years, the proportion of "virtual increase" in local fiscal performance has decreased, mainly due to economic downturn, tax reduction and exemption, local tax contraction, grassroots "three guarantees", local government debt repayment and interest payment, epidemic prevention and other factors leading to insufficient local fiscal liquidity. The budget is difficult to effectively balance, and it is necessary to raise fiscal funds through various forms. We should rationally view certain "irrational" behaviors of local finance in the current special period.

In recent years, due to the impact of the epidemic, large-scale tax refunds and reductions, and the sluggish real estate and land market, many local governments have seen a decline in fiscal revenue and intensified income and expenditure contradictions.

According to data from the Ministry of Finance, the local general public budget revenue at this level in China in 2022 was approximately 10.9 trillion yuan, a year-on-year decrease of 2.1%. In 2022, the budget revenue of local government funds in China, mainly from land sales, was approximately 7.4 trillion yuan, a year-on-year decrease of 21.6%. Affected by last year's low base, the local general public budget revenue in the first half of this year was about 6.5 trillion yuan, a year-on-year increase of 13.5%. The budget for local government funds at this level is about 2.2 trillion yuan, a year-on-year decrease of 17.2%.

How to rectify

The harm of inflating fiscal revenue is significant. In recent years, the Ministry of Finance has repeatedly ordered local governments not to inflate fiscal revenue and improve the quality of fiscal revenue.

Shi Zhengwen believes that the inflated fiscal revenue conceals the true fiscal revenue situation, conceals the actual fiscal deficit, exacerbates local fiscal risks, and also interferes with the central government's judgment of the true fiscal situation of local areas, which can easily mislead decision-making, affect macroeconomic regulation, and damage the government's credibility.

In addition, higher-level governments often rely on real financial resources as the basis for local transfer payments, while local governments inflate fiscal revenue, narrow the income and expenditure gap, thereby reducing the scale of higher-level government transfer payments, and actually reducing the available financial resources and livelihood guarantee capabilities of local governments.

How to prevent the false increase of fiscal revenue still requires multiple measures to address both the root cause and the root cause.

The chart is from Yuekai Securities Research Institute

The current economic situation is complex and complex. Experts believe that local governments should correct their views on political performance, be more cautious in determining income targets, scientifically and reasonably determine income targets, and implement budget laws and other income indicators as only expected indicators, rather than rigid task completion indicators, to reduce the false increase in local income in order to complete tasks.

Shi Zhengwen stated that some officials believe that inflating fiscal revenue is not just a matter of corruption for personal gain, and that punishment often involves warnings and demerits. Therefore, there is insufficient understanding of the harm of inflating fiscal revenue in terms of ideology. Therefore, to prevent the inflated fiscal revenue, officials need to deepen their understanding. In the current financial difficulties, it is necessary to strengthen supervision and accountability to prevent the trend of inflated fiscal revenue from rising. When necessary, relevant departments can conduct special inspections, analyze the causes, and take targeted measures to solve the problem.

The quality of current fiscal revenue has become one of the key contents of supervision by local regulatory agencies of the Ministry of Finance to curb the rise of local fiscal revenue fraud.

In February this year, the General Office of the Communist Party of China and the State Council issued the "Opinions on Further Strengthening Financial and Accounting Supervision", requiring that in strengthening financial and accounting supervision in key areas, serious investigations and punishments should be carried out on issues such as untrue and non compliant fiscal revenue. To implement this opinion, the Ministry of Finance has launched a special action on financial and accounting supervision and a special action on budget execution supervision.

Wang Zhenyu stated that inflating fiscal revenue not only addresses the symptoms but also focuses on addressing the root cause, scientifically and reasonably constructing a system that matches local fiscal powers with expenditure responsibilities, and correcting the practice of some remaining expenditure responsibilities being "bottom-up" at the grassroots level.

Last year, the General Office of the State Council issued a document to further promote the reform of the fiscal system below the provincial level, requiring the reasonable preparation of income budgets at all levels based on the actual tax sources, the collection of taxes and fees in accordance with laws and regulations, the strict implementation of tax refund and fee reduction policies, and the strict prohibition of false collection and transfer, excessive collection of taxes and fees, and arbitrary charging. It is not allowed to illegally assess and rank tax revenue indicators. Provincial-level governments can use reasonable adjustments to income sharing methods or ratios to curb behaviors such as false income and idle income.