What are the impacts on us?, Deposit interest rates have decreased in regions | banks | interest rates

01

Multiple banks have gradually lowered their RMB deposit interest rates

Recently, many banks have been adjusting their RMB deposit interest rates.

On June 8th, Industrial and Commercial Bank of China, Agricultural Bank of China, Bank of China, Construction Bank, Bank of Communications, and Postal Savings Bank of China, the six major banks, announced the first reduction in the RMB current deposit interest rate and some fixed deposit interest rates.

On June 12th, joint-stock banks such as China Merchants Bank, Shanghai Pudong Development Bank, CITIC Bank, Everbright Bank, and Zhejiang Commercial Bank followed the six major banks in lowering their RMB deposit interest rates.

Subsequently, several urban commercial banks, including Jiangsu Bank, Shanghai Rural Commercial Bank, Tongxiang Rural Commercial Bank, etc., as well as small and medium-sized banks such as Rural Commercial Bank and Rural Bank, have successively lowered their RMB deposit interest rates.

02

Different bank deposit interest rates vary

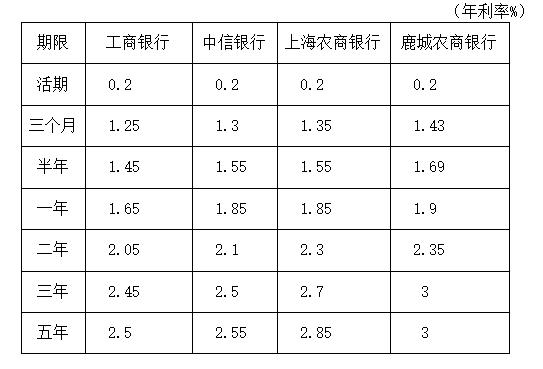

So what is the approximate level of RMB deposit interest rates for various banks now?

The reporter selected several different types of banks and compared their latest interest rates.

At present, the RMB deposit interest rates of the six major banks remain consistent, while the deposit interest rates of national joint-stock banks vary slightly, but the difference is not significant, overall slightly higher than the six major banks. The deposit interest rates of various urban commercial banks, rural commercial banks, rural credit cooperatives, and rural banks vary. Some are close to the interest rates of joint-stock banks, but some rural commercial banks and rural banks still have deposit products with annual interest rates of 3% or above.

03

The deposit interest rates of the same bank may also be different

The reporter's investigation also found that the listed interest rates published on various bank websites are all, but in reality, even for the same bank, the actual interest rates implemented by branches in different regions may vary. Regarding this, Zhao Tingchen, a researcher at the Bank of China Research Institute, stated that the regional deposit interest rate spread of the same bank is mainly influenced by three factors. One is related to the richness of savings tools for residents in different regions. If residents in a certain area have insufficient options for wealth management, funds, trusts, and other tools to choose from, and rely too much on deposits, it will increase the supply of deposits, leading to generally low interest rates for various banks in the region. The second is related to the degree of competition among financial institutions in different regions. If the competition among financial institutions in a certain area is relatively fierce, it may exacerbate the trend of "high interest deposit solicitation", leading to generally high deposit rates among local banks. The third is related to the depth of financial institutions' roots in different regions. The same bank may have a larger number of branches and higher recognition from depositors in certain regions, while its customer base in other regions is weak, which may lead to the bank needing to attract deposits at different interest rates in different regions.

04

"Inter provincial deposits" are just an isolated phenomenon

In addition, there has been a phenomenon of "inter provincial deposits" in some regions recently. Some customers who are sensitive to changes in deposit interest rates withdraw cash from their original banks and choose banks with higher interest rates in neighboring areas or even across provinces to deposit. Regarding this phenomenon, Zhao Tingchen believes that the emergence of "inter provincial deposits" itself reflects the free flow of funds on a larger scale, and does not contradict the policy orientation of building a "unified large market" in China, nor does it violate discipline and rules. Therefore, this phenomenon itself is understandable. However, for depositors, cross provincial deposits will incur transportation and labor costs. Conducting large-scale cash transfers also poses security risks. If the deposit amount is small, it may not be economical enough. Therefore, "inter provincial deposits" should only be an isolated phenomenon.

05

Why did the bank lower the RMB deposit interest rate?

We usually choose banks with higher interest rates for deposits, so why are so many banks lowering their deposit rates?

Firstly, banks are also enterprises. As a financial enterprise, net interest margin is one of the important indicators to measure the profitability of banks. Loans, bond investments, and interbank assets are all interest bearing assets of a bank, and the ratio of a bank's net interest income to all interest bearing assets is called the net interest margin.

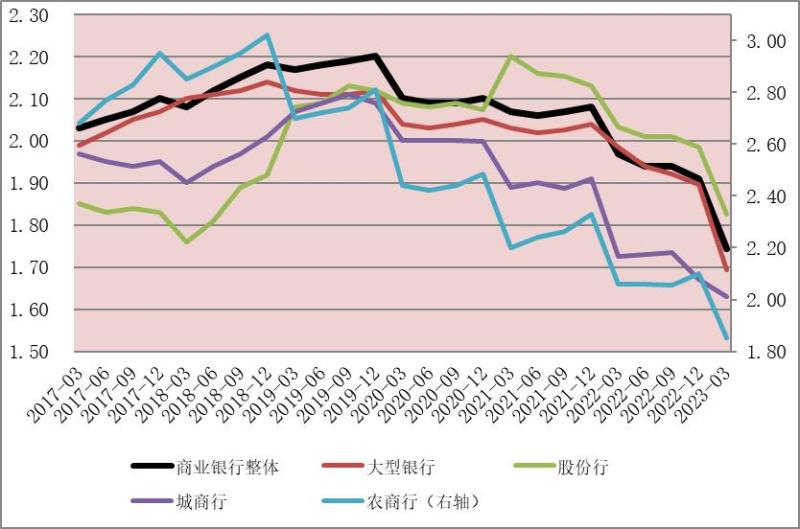

According to data released by the State Administration for Financial Regulation, the net interest margin of commercial banks in 2022 showed a quarterly decline, with a year-end net interest margin of 1.91%, a year-on-year decrease of 17 basis points. However, the net interest margin in the first quarter of 2023 was only 1.74%, a decrease of 0.17 percentage points from the fourth quarter of 2022, setting a new historical low.

The trend of changes in net interest margin of commercial banks

Zeng Gang, Deputy Director of the National Finance and Development Laboratory, stated that according to the "Implementation Measures for Qualified Prudent Assessment" previously released by the market interest rate pricing self-discipline mechanism, the "warning line" for the net interest margin rating is 1.8%, and scores below 1.8% will be deducted. Banks have reached the point where they must fight to protect interest margins. Therefore, various commercial banks have lowered their deposit interest rates to meet their net interest margin management needs. At the same time, as the overall market loan interest rates have significantly decreased, commercial banks can flexibly adjust deposit interest rates, which is also a normal response mechanism for commercial banks in the market-oriented environment of deposit interest rates.

Regarding the different interest rate levels adjusted by various banks, Zeng Gang believed that small and medium-sized banks have high capital costs and narrow financing channels. A significant reduction in deposit interest rates will lead to difficulties in debt business and tightening liquidity. Therefore, small and medium-sized banks can maintain deposit interest rates slightly higher than large banks to maintain a certain level of reserve attraction competitiveness.

06

What is the impact of the decrease in RMB deposit interest rates?

Experts point out that the decline in deposit interest rates is largely influenced by the decline in loan interest rates, but the decline in deposit interest rates will in turn affect the level of loan interest rates. The June loan market quoted interest rates announced on the 20th: both 1-year and 5-year and above have decreased by 10 basis points, which is also partly related to the decline in deposit rates. On the 20th, several banks in Shanghai announced a reduction in mortgage interest rates. The loan interest rate for the first home was lowered from 4.65% to 4.55%, and the loan interest rate for the second home was lowered from 5.35% to 5.25%. Savers who need to buy a house can save a lot of loan interest.

Of course, the most direct impact of the reduction in bank deposit interest rates is that residents' deposit interest income has decreased, but the magnitude of the decrease is not significant. Taking Industrial and Commercial Bank of China as an example, the interest rates for three-month, six-month, and one-year fixed deposits have not been adjusted. The largest adjustment is for five-year fixed deposits, with the annual interest rate reduced from 2.65% to 2.5%, a 15 basis point decrease. Equivalent to a deposit of 10000 yuan, the annual interest has decreased by 15 yuan.

Of course, the deposit interest has decreased, so we should be able to optimize asset allocation.

For residents who have a strong interest in savings or have minimal risk tolerance, bank deposits are undoubtedly the best choice. Of course, large certificates of deposit from banks are a better choice, and their interest rates may be higher than the pre adjusted fixed deposits. In addition, treasury bond is also a safe choice, and its yield is higher than that of ordinary time deposits.

In addition, for residents with certain risk tolerance, bank wealth management and insurance products are also options for diversified investment. The reporter learned from the Banking Wealth Management Registration and Custody Center that at the end of April this year, the total scale of bank wealth management increased by 1.26 trillion yuan compared to the end of March, and the total scale continued to increase by the end of May. Meanwhile, since the beginning of this year, the average yield of bank wealth management products has been the lowest at 2.95% and the highest at 4.36%, which is much higher than the deposit interest rate. It indicates that some depositors have increased their investment in bank wealth management. Dong Ximiao, a researcher at the Financial Research Institute of Fudan University, believes that the increase in the size of the bank's wealth management market can basically be regarded as the "return" of deposits.

Here is a tip: Before investing in wealth management products, it is important to take the bank's risk tolerance test seriously and not purchase investment products that exceed your own risk tolerance.

Of course, residents with high risk tolerance can also participate in investments such as funds, stock markets, and gold investments. However, investment carries risks and we must not forget that the safety of funds is always more important than the possible rate of return.