The offshore RMB once fell below 7.3! The US dollar index surged above 103, ignoring the median signal index | US dollar | offshore

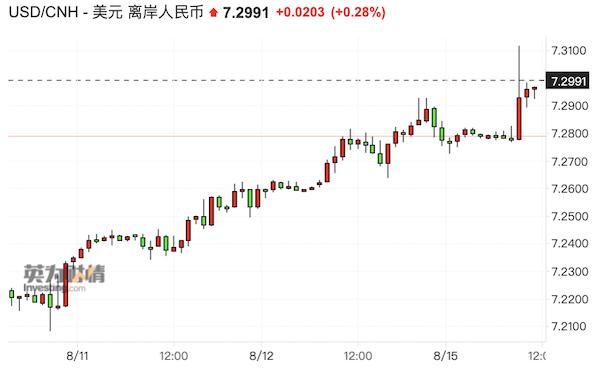

On August 15th, the offshore renminbi fell to its weakest point against the US dollar around 7.31, followed by trading at 7.29; The onshore RMB trend is relatively strong. Traders told reporters that the stability signal of the middle price is strong, and the impact of countercyclical factors has exceeded 700 points in recent days. However, the exchange rate still fell to around 7.25 on the 15th. On that day, the central bank's reverse repo rate and MLF rate were "reduced" by 10BP and 15BP respectively.

On the one hand, in recent times, the US dollar index has continued to rebound, rising to 103 overnight, and the 10-year US bond yield has approached 4.2%, helping the US dollar index to close higher for four consecutive weeks; On the other hand, the continuous widening of the interest rate spread between China and the United States has intensified the pressure on the depreciation of the renminbi.

On the 15th, economic data such as total retail sales of consumer goods, growth rate of fixed investment, industrial added value, and unemployment rate for July were released, which fell short of expectations.

The US China interest rate spread exacerbates the pressure on RMB depreciation

Traders and analysts told reporters that on August 14th, the median price of the Chinese yuan against the US dollar was 7.1686, the closing price was 7.2537, and the impact variable of the countercyclical factor was -791 basis points; On the 15th, the model predicted a median price of 7.2598 and reported a median price of 7.1768. The stability signal released by the middle price is strong.

However, after the opening on the 15th, the renminbi weakened significantly, with the onshore and offshore price difference widening to around 500-700 points. Offshore bearish sentiment was stronger, and hedge fund short positions had already been at a high level. Carry trading was the main reason for the pressure on the renminbi. A foreign exchange analyst at a foreign bank previously told reporters that traders had previously hedged interest rates by holding US dollars and selling Chinese yuan, and then began to hedge interest rates by long selling Singapore dollars against Chinese yuan.

Over the past week, market sentiment has been affected - stimulus policies have not been effectively implemented, Country Garden has overdue payment of US dollar bond interest, and export, inflation, and social financing data are lower than expected. In this context, traders are generally concerned about the July economic data released on the 15th, but the data still falls short of expectations.

According to data released by the Bureau of Statistics, the total retail sales of consumer goods in July increased by 2.5% year-on-year, with a previous value of 3.1%; The added value of industrial enterprises above designated size increased by 3.7% year-on-year, with a previous value of 4.4%; From January to July, urban fixed assets investment increased by 3.4% year on year, expected to be 3.7%, with the previous value of 3.8%; From January to July, the national real estate development investment increased by -8.5% year-on-year, with an expected -8.1% and a previous value of -7.9%; The urban survey unemployment rate in July was 5.3%, with an expected 5.2%, compared to the previous value of 5.2%. The Bureau of Statistics stated that starting from August, the unemployment rate survey for young people in urban areas will be discontinued.

"As the Federal Reserve's interest rate hike cycle comes to an end, it was previously expected that the US China interest rate spread may narrow, but unexpectedly, the situation is developing in the opposite direction, leading to increased exchange rate pressure," said the trader.

On the one hand, US bond interest rates have recently skyrocketed again. After the downgrade by Fitch, the 10-year US bond yield has exceeded 4.1%. The sluggish demand for US bond auctions and higher than expected PPI have pushed up yields for various maturities, helping the US dollar index to close higher for four consecutive weeks; On the other hand, due to a slower than expected recovery, China has instead started a cycle of interest rate cuts, leading to an increase in the magnitude of the inverted interest rate spread between China and the United States.

On the 15th, the central bank lowered the policy interest rate - the 7-day reverse repurchase operation rate was 1.8%, a decrease of 10BP from the previous month; The MLF operating rate is 2.5%, a decrease of 15BP from the previous month. This is another policy cut by the central bank after the interest rate cut in June, and the current expectation of reserve requirement reduction is also strong.

Wang Yunjin, Senior Researcher at Zhixin Investment Research Institute, told reporters that given that the net interest margin of the banking system has dropped to around 1.7%, the narrow profit margin has reduced its enthusiasm for credit investment. In order to reduce social financing costs, the first step is to reduce the bank's debt costs, among which reducing the OMO and MLF interest rates is a more appropriate choice. In the future, it may speed up the pace of issuing treasury bond and local bonds, and moderately pushing down interest rates will also help reduce the debt burden of local governments.

Real estate issues remain the focus

The trend in the real estate sector is still the focus of attention from all parties. Last week, the net outflow of northbound funds exceeded 25 billion yuan per week, and on the morning of the 15th, the net outflow exceeded 5 billion yuan, which also partially caused pressure on the exchange rate.

Last week, Country Garden failed to pay the $22.5 million coupon on two international bonds as scheduled. This news has had an impact on the already weak Chinese real estate industry.

Nomura China's Chief Economist, Lu Ting, stated in an email to reporters that there is a view that the debt risk of Country Garden may not be as severe as Evergrande's default, as Country Garden's interest bearing debt and total debt are only 44% and 59% of Evergrande's. However, US dollar bonds and onshore bonds are only a small part, and the key is not to ignore Country Garden's largest creditor - homeowners waiting to deliver their homes, who account for a significant portion of Country Garden's total debt, reaching 47%, while Evergrande's proportion is 38%.

Country Garden's business is highly concentrated in lower tier cities, which accounted for 68% of its new home sales in 2021. According to Country Garden's 2022 annual report, the company has 3121 ongoing projects covering 1401 towns in 31 provinces.

International institutions are highly concerned about the Chinese real estate market. Lu Ting stated that in 2020, the real estate industry contributed 38.0% of local government revenue, of which 7.2% came from real estate related taxes and 30.8% came from land sales revenue. Due to the sluggish real estate market in 2022, this proportion has dropped to 30.8%, mainly due to the contraction of land sales revenue, which has decreased to 23.9%.

The short-term momentum of the US dollar rebounds

In the future, the direction of the US dollar is also closely related to the exchange rate of the Chinese yuan. A few weeks ago, the US dollar index fell to the 99 range. The expectation of the Federal Reserve suspending interest rate hikes prompted traders to significantly long for the Japanese yen and euro. However, the economic weakness in the eurozone far exceeded expectations, and the hawkishness of the Bank of Japan fell short of expectations. This has led to the US dollar index continuing to rebound in recent weeks, standing at 103 overnight.

Jerry Chen, senior analyst at Jiasheng Group, told reporters that the US CPI rebounded in July, ending 12 consecutive declines, but the growth rate was lower than expected, and the core CPI dropped from 4.8% to 4.7%. Inflation is still moving in the right direction. Although this means that the necessity of interest rate hikes has decreased, the recent University of Michigan Consumer Confidence Index has been better than expected, indicating a significant decrease in the probability of a US recession. Coupled with the rising 10-year US Treasury yields, this has helped the US dollar index continue to rise for four consecutive weeks. Non US currencies were completely wiped out last week, and the US dollar/day rose to near its previous high of 145. The euro, Australian dollar, Canadian dollar, and other currencies have fallen for four consecutive weeks.

"The Federal Reserve raised interest rates by 25BP at its July meeting, but did not rule out the possibility of a rate hike in September. This week, attention needs to be paid to whether there will be more and more hawkish voices in the meeting minutes. Data is the basis for future decisions. Currently, the market's expected probability of a rate hike in September is less than 10%, and it is around 30% in November. This week's economic data in the United States focuses on Tuesday's retail sales, with an expected month on month growth rate of 0.4% from 0.2%.".

"From a technical perspective, the rebound of the US dollar for four consecutive weeks has approached the March downward trend resistance line. The upper resistance targets are concentrated at the closing price of the 2023 weekly high, the 52 week moving average, and the 38.2% retracement level of 105.39 for the 2022 decline - if this is reached, there will be a greater upward trend. The lower support level is 101.08."

However, the current consensus expectation on Wall Street is that the US dollar will peak, and the key is when the US dollar will actually weaken and how much it will weaken. This is often the most difficult to predict.