Sudden! Agricultural Bank of China, Minsheng Bank and other "planted" enterprises | Loans | Agricultural Bank of China

On August 18th, the official website of the State Administration for Financial Regulation released several administrative penalty information. Minsheng Bank, Agricultural Bank of China, Guangfa Bank, China Huarong, and Oriental Asset Management have all been issued large fines for violating relevant regulations, totaling over 130 million yuan.

Minsheng Bank fined 47.8 million yuan

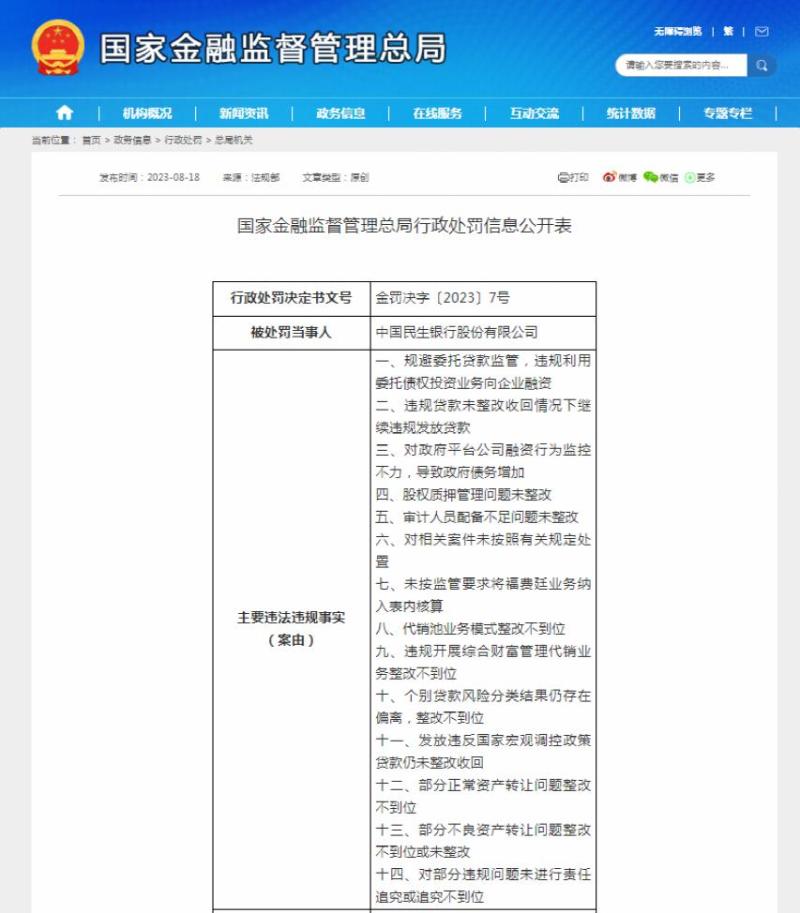

The Administrative Penalty Information Disclosure Form shows that China Minsheng Bank was fined a total of 47.8 million yuan by the State Administration of Financial Supervision for violating Article 21 and Article 46 of the Banking Supervision and Administration Law of the People's Republic of China and relevant prudent business rules. Among them, the head office is 44.3 million yuan, and the branch offices are 3.5 million yuan.

There are a total of 14 main illegal and irregular facts in this bank. Specifically, it includes:

Evading supervision of entrusted loans and illegally using entrusted debt investment business to finance enterprises;

Continuing to issue loans in violation of regulations without rectification and recovery;

Inadequate monitoring of financing behavior by government platform companies has led to an increase in government debt;

The issue of equity pledge management has not been rectified; The issue of insufficient staffing of auditors has not been rectified;

Failure to dispose of relevant cases in accordance with relevant regulations;

Failure to include Forfaiting's business in on balance sheet accounting in accordance with regulatory requirements;

The rectification of the consignment pool business model is not in place;

Inadequate rectification of illegal implementation of comprehensive wealth management consignment business;

There are still deviations in the classification results of individual loan risks, and the rectification is not in place;

Loans issued in violation of national macroeconomic regulation policies have not been rectified and recovered;

Insufficient rectification of some normal asset transfer issues;

The transfer of some non-performing assets has not been properly rectified or not rectified;

Failure to hold accountable or inadequate accountability for certain violations.

In addition, Bai Dan, the then Secretary of the Board of Directors of China Minsheng Bank Co., Ltd., was responsible for the failure to rectify the equity pledge management issues of Minsheng Bank and was issued a warning by the State Administration of Financial Supervision.

Agricultural Bank of China fined 44.2 million yuan

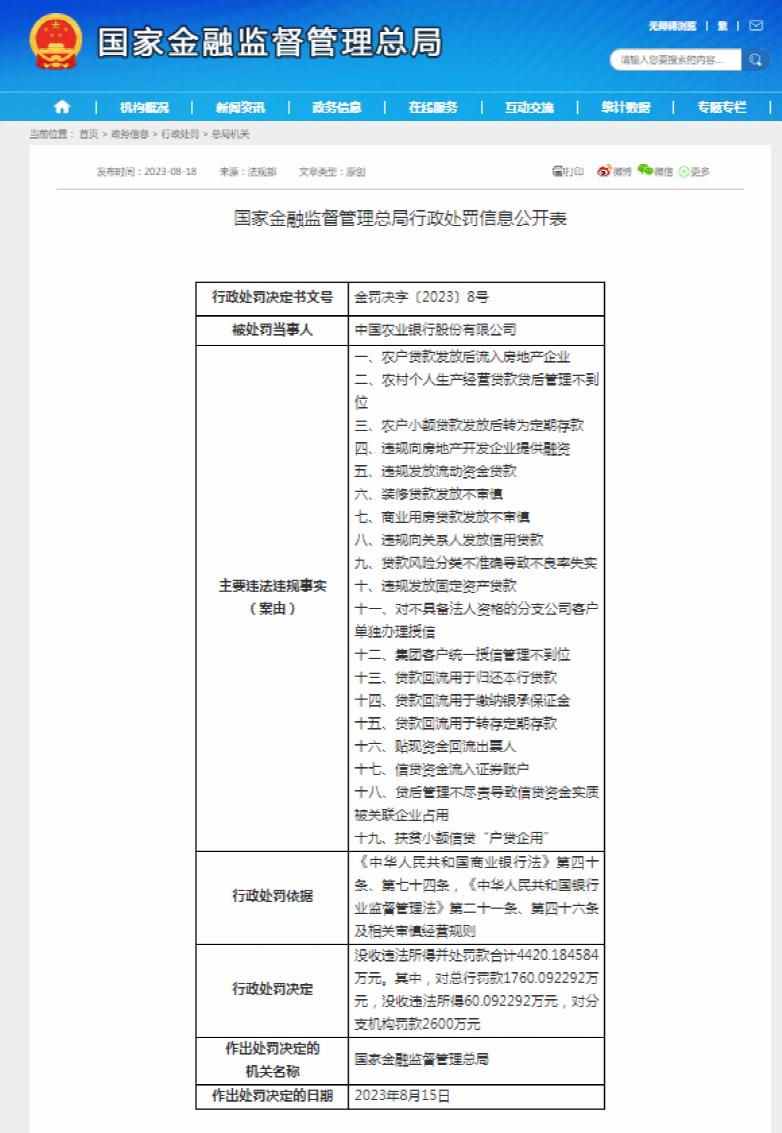

The Administrative Penalty Information Disclosure Table shows that Agricultural Bank of China Co., Ltd. has been confiscated of illegal gains and fined a total of 44.20.18 million yuan by the State Administration of Financial Supervision for violating Articles 40 and 74 of the Commercial Bank Law of the People's Republic of China, Articles 21 and 46 of the Banking Supervision and Administration Law of the People's Republic of China, and related prudent business rules. Among them, a fine of 17.609 million yuan was imposed on the head office, illegal gains of 6.009 million yuan were confiscated, and branch offices were fined 26 million yuan.

There are a total of 19 main illegal and irregular facts in this bank. Specifically, it includes:

After the issuance of farmer loans, they flow into real estate enterprises;

Inadequate post loan management for rural personal production and operation loans;

After the issuance of small-scale loans for farmers, they are converted into fixed deposits;

Illegally providing financing to real estate development enterprises;

Illegally issuing working capital loans;

Inappropriate disbursement of renovation loans;

Inappropriate issuance of commercial housing loans;

Illegally issuing credit loans to related parties;

Inaccurate classification of loan risks leads to inaccurate non-performing loan ratios;

Illegally issuing fixed asset loans;

Apply for separate credit for branch company clients who do not have legal personality;

Inadequate unified credit management for group clients;

The loan return is used to repay the bank's loan;

The loan repayment is used to pay the bank guarantee deposit;

The loan return is used for depositing fixed deposits;

Discounted funds flowing back to the issuer;

Credit funds flow into securities accounts;

Inadequate post loan management resulted in the substantial occupation of credit funds by affiliated enterprises;

Small scale poverty alleviation loans for households and enterprises.

Guangfa Bank fined 23.4 million yuan

The administrative penalty information disclosure form shows that Guangfa Bank was fined a total of 23.4 million yuan by the State Administration of Financial Supervision for violating Article 20, Article 21, Article 46 of the Banking Supervision and Administration Law of the People's Republic of China and relevant prudent business rules. Among them, the head office is 5.5 million yuan, and the branch offices are 17.9 million yuan.

There are a total of 14 main illegal and irregular facts in this bank. Specifically, it includes: inaccurate classification of small and micro enterprises; Illegally issuing real estate loans; Illegally issuing working capital loans; Illegally issuing land reserve loans; Illegally issuing loans to enterprises for land reserve projects; Fulfilling the duties of senior management personnel without qualification approval; Not providing unified credit to group customers; The quality of credit assets is not reflected truthfully; Credit funds illegally flow into securities accounts; Loan funds illegally flow back to borrowers; Failure to strictly implement entrusted payments; Falsely increasing the scale of deposits and loans; Credit card overdraft funds flow into real estate development enterprises; The management of merger and acquisition loans is not standardized.

China Huarong fined 14.23 million yuan

The administrative penalty information disclosure form shows that China Huarong Asset Management Co., Ltd. has violated Article 18, Article 19, Article 45 and other provisions of the Banking Supervision and Administration Law of the People's Republic of China by illegally investing in non-public issuance of stocks; Fined 7.1191 million yuan by the State Administration for Financial Regulation, confiscated 7.1191 million yuan of illegal gains, and confiscated a total of 14.2383 million yuan.

Dongfang Asset was fined 5.3 million yuan

The administrative penalty information disclosure form shows that China Eastern Asset Management Co., Ltd. was fined a total of 5.3 million yuan by the State Administration of Financial Supervision for violating Article 21 and Article 46 of the Banking Supervision and Administration Law of the People's Republic of China and relevant prudent business rules. Among them, the head office is 4.3 million yuan, and the branch offices are 1 million yuan.

The main illegal and irregular facts include: providing financing to enterprises under the pretext of acquiring non-performing debts; Non clean acquisition of non-performing debts; Violating regulations to evade concentration supervision through collaborative business within the group.