Promote direct preferential policies and introduce new policies on tax and fee incentives for buying a house? State Administration of Taxation: Policy sorting and collection for querying State Administration of Taxation | Taxation | State Administration of Taxation

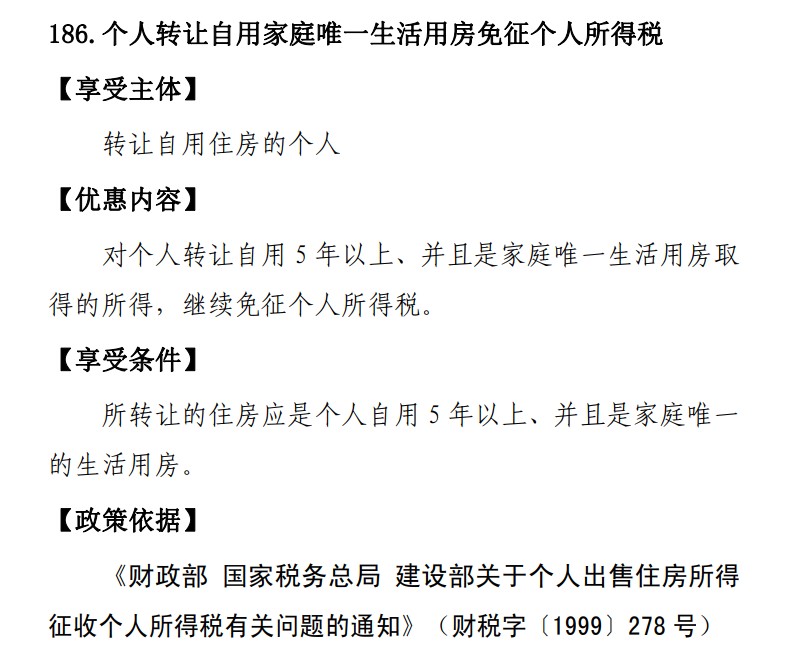

Is there a new tax policy for buying and selling houses? Can the transfer of the only residential property within five years be exempt from personal income tax? On July 25th, the official website of the State Administration of Taxation released the "Guidelines for Supporting Coordinated Development of Tax and Fee Preferential Policies", which included 19 tax and fee preferential policies related to the real estate sector. After the release of the "Policy Guidelines", it triggered multiple interpretations in the market.

On July 26th, Pengpai News consulted the tax consultation hotline of the State Administration of Taxation and industry insiders, stating that the new policy on tax and fee for buying and selling houses has not been released, only a review of previous tax and fee preferential policies.

Yan Yuejin, Research Director of E-House Research Institute, stated that the relevant content does not belong to the latest released policies, but rather to policies that have been continuously implemented in the past few years. This should be understood as a review, summary, and further promotion of many preferential policies, in order to better release the signal and guidance of loose tax and fee policies.

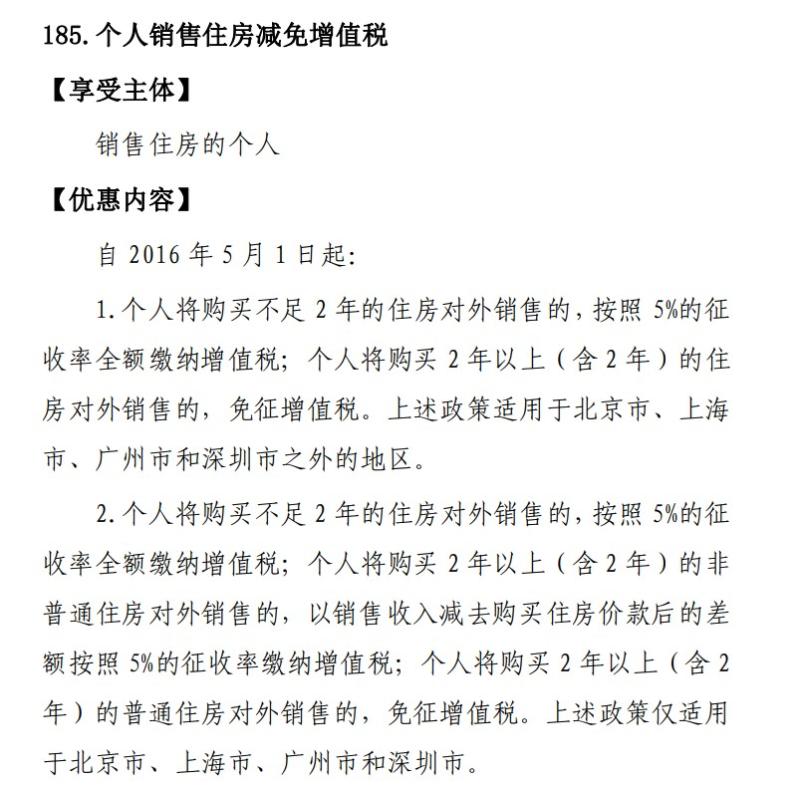

At present, the market is more concerned about topics such as reducing value-added tax on personal housing sales, exempting personal income tax on personal transfer of the only household living space for personal use, reducing deed tax on personal purchase of the only household or second improved housing, and refunding personal income tax for residents who purchase replacement housing.

This has also led to market misunderstandings, including exemption from personal income tax for transferring only residential properties within five years, exemption from value-added tax for properties under two years, and exemption from value-added tax for non ordinary housing listed for trading for more than five years.

Regarding this, the relevant staff of the tax consultation hotline of the State Administration of Taxation stated that the policy guidelines mainly sorted out the tax and fee preferential policies. The specific preferential content and conditions are clearly stated in the "Compilation of Guidelines for Supporting Coordinated Development of Tax and Fee Preferential Policies", such as the item "Personal Income Tax Exemption for Personal Transfer of Household Only Living House", which still requires that the transferred housing should be for personal use for more than 5 years and be the only living house of the family.

The conditions for reducing value-added tax on personal housing sales have not been adjusted. Individuals who purchase housing for less than 2 years and sell it to the public shall pay value-added tax in full at a rate of 5%; Individuals who purchase housing for more than 2 years for external sales are exempt from value-added tax. For first tier cities, individuals who purchase non ordinary housing for more than 2 years for external sales shall pay value-added tax at a rate of 5% based on the difference between the sales revenue and the purchase price of the housing.

The policy of refunding personal income tax for residents who purchase alternative housing has also been released in 2022. According to regulations, from October 1, 2022 to December 31, 2023, taxpayers who sell their own housing and purchase new housing in the market within one year after the sale of their current housing will be eligible for a tax refund on the personal income tax already paid on the sale of their current housing. Among them, if the amount of newly purchased housing is greater than or equal to the current housing transfer amount, all personal income tax already paid will be refunded; If the amount of newly purchased housing is less than the transfer amount of the current housing, the personal income tax already paid for the sale of the current housing shall be refunded according to the proportion of the newly purchased housing amount to the transfer amount of the current housing.

In addition, an article released by the official WeChat account of the State Administration of Taxation shows that the State Administration of Taxation has recently released the "Guidelines for Supporting Coordinated Development of Tax Preferential Policies" and "Guidelines for Supporting Shared Development of Tax Preferential Policies". The two guidelines focus on the two main themes of "coordination" and "sharing", respectively. According to the writing format of the beneficiaries, preferential content, conditions, and policy basis, the tax preferential policies supporting coordinated development and shared development are sorted and collected, making it easier for taxpayers of different types to access and query, and promoting the direct and fast enjoyment of tax preferential policies.

Among them, the "Guidelines for Coordinated Development" have summarized and formed 216 tax and fee preferential policies that support coordinated development. Taxpayers can access the website of the State Administration of Taxation according to their actual needs, check, download, and compare operations on their own, apply tax and fee preferential policies that are suitable for their own development, and fully enjoy the policy dividends.

The person in charge of the Policy and Regulations Department of the State Administration of Taxation stated that the tax department will update and improve new tax and fee preferential policies in a timely manner based on the existing policy guidance system, continuously increase policy promotion and guidance efforts, and continuously improve the implementation of tax and fee policies, so that taxpayers and payers can understand the policies, know how to operate, enjoy, and feel more.