Is the US economy facing new tests and rebounding again? The process of anti inflation has entered a difficult area. The United States | consumers | economy

On Thursday local time, the United States will release July Consumer Price Index data.

As a key factor in the future policy decisions of the Federal Reserve, the inflation path will have a significant impact on when the current tightening cycle will end. The latest institutional forecast shows that this month's data will return to over 3%, and the slow cooling of inflation and slowing economic expansion in the next stage will create another major challenge - stagflation, which will have a new impact on the financial market.

The process of anti inflation may encounter challenges

Since hitting a nearly 40 year high in mid-20th last year, US inflation has gradually slowed down under the tough policy stance of the Federal Reserve. In June, the overall CPI only increased by 3.0% year-on-year, marking a new low since March 2021. The significant decline in growth rate can be largely attributed to a slowdown in food inflation and a significant drop in energy prices compared to the high point in the summer of 2022.

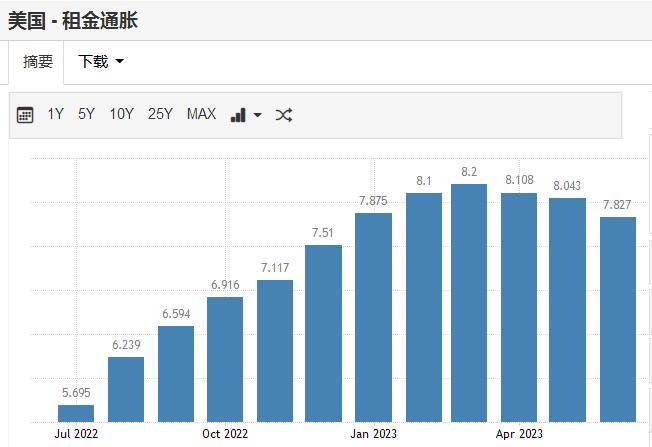

In July, industry data showed that deflation in used cars and goods is expected to continue. At the same time, the rise in rent may further slow down, with the Apartment List national rent index rising only 0.3% month on month in July, which is often the highest point of seasonal rent growth. Due to the increase in supply and weak demand, the rental growth rate in 2023 is significantly lower than the seasonal trend in previous years.

The inflection point of US rent inflation may be clear

However, the base effect of energy prices will weaken, and the rise in US gasoline prices in recent weeks may become an uncertain factor for inflation. Institutions predict that the overall CPI may slightly rebound to 3.3% last month.

As a core inflation indicator that the Federal Reserve is more concerned about, it may continue to be high fever. In the hot labor market environment, inflation in the service industry remains challenging, and prices of tourism and medical services still face significant upward pressure. According to institutional forecasts, the core CPI increased by 4.7% year-on-year last month, with a growth rate only falling by 0.1 percentage points.

Oanda Senior Market Analyst Erram said in an interview with First Financial reporters that the worst stage for inflation has passed. After demand suppresses commodity inflation, the cooling of rental inflation will gradually become apparent. He believes that the lagging effect of monetary policy in the second half of the year will continue to suppress prices, but compared to the past year, the decline will be slower and even more volatile.

The New York Federal Reserve reported on Tuesday in the Quarterly Report on Household Debt and Credit that the US credit card debt exceeded $1 trillion, and despite rising interest rates, consumers continued to consume, which could complicate the Fed's task of cooling the economy and curbing inflation. Federal Reserve officials also seem to have no intention of slowing down the pace of tightening in their latest speeches. Philadelphia Fed Chairman and this year's FOMC voting committee member Huck said this week, "If there are no worrying new data from now until mid September, I believe we may have patience to keep interest rates stable and let monetary policy action take effect."

Erram told First Financial Analysis that for the Federal Reserve, high core inflation remains a significant policy adjustment. The key to the inflation outlook is the labor market and nominal wage growth. At present, the salary growth rate has slowed down compared to last year's high, but still far exceeds the interest rate that is consistent with the Federal Reserve's inflation target. Before the labor market weakens, the Federal Reserve may continue to take a tough stance.

Is stagflation approaching

Despite the Federal Reserve's proactive tightening policies, the main components of the economy have performed better than expected in recent months. Data shows that driven by stable consumer spending and a rebound in business investment, the US economy expanded at an annual growth rate of 2.4% in the second quarter, reigniting confidence in a soft landing for the economy.

However, this may be a potential critical point. The Federal Reserve's Brown Book states that with further release of monetary policy effects, the expectation for economic activity in the coming months is to continue to slow down. If inflation cannot quickly fall, stagflation may become a potential problem facing the US economy. The July non farm payroll data may be a signal, with only 187000 new jobs added in the United States, the smallest increase since December 2020, and the previous month's data also showing a significant downward revision.

Jacobson, Chief Investment Officer of Shengbao Bank, has issued a warning that stagflation will begin in the fourth quarter and will truly have a significant impact in the first and second quarters of next year. Jacobson said that as the US Treasury Department increased the issuance of treasury bond bonds, the market fell into "debt indigestion". "High deficit financing and chain issuance are in line with the cyclical rise of US real interest rates. The premise is that the deflationary real interest rate of endless financing is negative, and now our real interest rate is positive," he said.

After the Biden administration avoided catastrophic debt defaults, the United States is now raising $5 billion a day to make up for its finances. However, the complex macro environment has also put the Federal Reserve in a dilemma. On the one hand, it needs to achieve the inflation target through monetary policy, and on the other hand, the impact of the interest rate level on the yield of treasury bond may become the trigger for a new round of crisis in the future. "We have reached a point where the 'carry over cost' is increasing exponentially, as there is no prospect of significant debt reduction or interest rate/inflation reduction. Now, mortgage rates are 7%, and new car and credit card rates are also rising," Jacobson said.

This will pose a huge challenge for business operations, with a decrease in profit growth rates, but input costs such as wages continue to rise. Jacobson expects that the full impact of this shift will be evident when Q3 performance is announced in the fourth quarter of this year. In this situation, the S&P 500 index will test support around 4050 points.

Bank of America has temporarily abandoned its recession forecast and believes that the atmosphere of stagflation is approaching: slow growth, persistent inflation, rising interest rates and bond yields. The bank wrote in its latest report that prices of industrial products, food, and other aspects are soaring from 22 year lows, with iron ore rising by 41%, sugar rising by 47%, gasoline rising by 39%, beef rising by 38%, cotton rising by 21%, and US housing prices rising by 14%... These are just basic elements of life.

Bank of America believes that even after the most aggressive tightening cycle in nearly forty years, there is still a significant weight anchored in institutional investment portfolios in the past low inflation, moderate growth, and low interest rate environments of around 2%. The current risk is that investors may not anticipate the sustainability of interest rates around 5%, which may ultimately have an adverse impact on high debt assets such as technology growth stocks. Therefore, the bank suggests that investors should pay attention to undervalued opportunities in sectors such as metals and energy.