International institutions have adjusted GDP forecasts again, with offshore RMB falling below 7.2 expectations | Economy | GDP

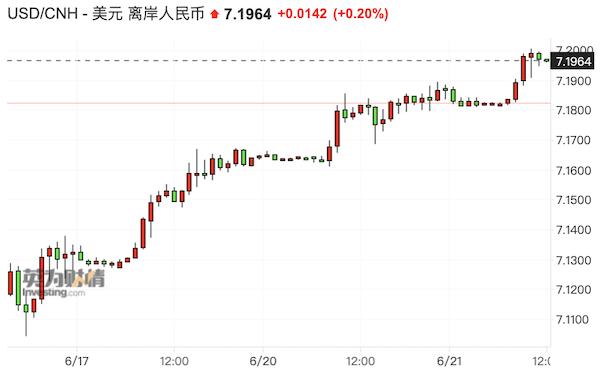

On the morning of June 21st, the offshore renminbi briefly fell below the 7.2 level against the US dollar, marking the first time since November last year. As of 12:00 Beijing time on the same day, the US dollar/People's Daily was at 7.1939, the US dollar/offshore RMB was at 7.1966, and the US dollar index was at 102.153.

First Financial has previously reported multiple times that the high interest rate spread between China and the United States, weak willingness of exporters to settle foreign exchange, and dividend payments from overseas Chinese listed companies have all led to high seasonal pressure on the renminbi. In addition, although the Federal Reserve suspended interest rate hikes in June, most institutions predict that there may be 1-2 more rate hikes starting in July.

"I haven't seen any obvious signs of intervention recently, it's just market-oriented depreciation," a trader from a foreign bank told reporters. "The exposure to overseas carry trades is high, and exporters don't choose to settle foreign exchange when it's not necessary. Coupled with the pressure of dividends, the RMB generally faces relatively high seasonal pressure in the second and third quarters." He also said that before and after the Spring Festival this year, the RMB appreciated significantly, which was also due to the concentration of foreign exchange settlement by exporters. ".

Barclays foreign exchange and macro strategist Zhang Meng told reporters that the latest forecasts for the US dollar/RMB are 7.2, 7, 6.9, and 6.8, respectively. In the future, the timing and intensity of China's policy relaxation measures may determine the performance of the exchange rate.

Recently, due to weak high-frequency data and weak external demand, many institutions have begun to adjust their GDP forecasts, but they are generally still higher than the official targets set by China. As early as the first quarter, due to high market expectations for economic recovery, coupled with economic data driven by base effects, many international institutions adjusted their GDP forecasts for 2023 to over 6%.

Over the weekend, Goldman Sachs lowered its 2023 GDP forecast for China from 6% to 5.4%; UBS announced on Tuesday that it will lower its GDP forecast for 2023 to 5.2%; Nomura announced last week that it will lower its GDP forecast for 2023 from 5.3% to 5.1% and its forecast for 2024 from 4.2% to 3.9%; Barclays predicts a GDP of 5.2% for 2023.

"We believe that the year-on-year growth rate of GDP in the second quarter may slow to between 1-2%, weaker than our previous expectation of 4.5%. With increased policy support, we still expect consumption to further recover moderately in the third quarter, real estate activity may stabilize, and economic growth to accelerate again. However, policy support may be relatively moderate, driving the economy to rebound moderately to 4-4.5% in the second half of the year, but it is unlikely to completely offset the impact of the economic weakness in the second quarter. Therefore, we have lowered our GDP growth forecast for 2023 to 5.2%, and our 2024 forecast to 5%."

In her view, the predicted downside risks mainly come from the uncertainty of the real estate market trend and loose policies, as well as the risk of a significant weakening of external demand. The timing, scale, and effectiveness of policy support may also pose certain downward risks.

Nomura China Chief Economist Lu Ting told reporters that the Chinese government is expected to launch a series of supportive measures after last week's interest rate cut. However, due to factors such as boosting confidence and emotions, declining land sales, etc., there is financial pressure and the transmission channels need to be unblocked. Therefore, the effectiveness of relevant measures needs to be observed.

Recent data shows that as the base effect subsides, the year-on-year growth rate of economic data in May has slowed down. The year-on-year growth rate of social consumer goods retail has slowed down to 12.7%, but its absolute level has slightly increased compared to April; Real estate sales have weakened to a year-on-year decrease of 3%, with new construction falling another 27%. However, after seasonal adjustments, real estate sales and new construction area have remained roughly unchanged or slightly increased compared to April, but are still at a weak low level; The year-on-year growth rate of infrastructure investment has accelerated to 8.8%, while the year-on-year growth rate of manufacturing investment has roughly stabilized; In May, exports fell by 7.5% year-on-year, and the momentum of month on month growth also weakened.

Wang Tao believes that if the economic growth momentum further weakens, future policy support may include: further relaxing real estate policies, such as further relaxing restrictions on purchasing houses in second tier cities, lowering down payment requirements for second home loans, increasing funding support for "guaranteed delivery of buildings," and improving financing conditions for developers; Enhance fiscal and quasi fiscal expansion efforts, such as accelerating the issuance of local government special bonds, raising and using a new batch of policy bank special infrastructure investment funds, in order to boost infrastructure investment; The central government can provide temporary credit and financial support to local governments to settle their debts to enterprise suppliers; But the possibility of the central government directly distributing large-scale consumption or income subsidies to residential sectors is very small; Further minor interest rate cuts, increased credit support to support the expansion of quasi fiscal policies, and restructuring or replacing local government financing platform debt with lower cost debt.

Mainstream institutions generally believe that some policy measures may be introduced before the end of July, but significant fiscal policy support and macroeconomic policy shifts may need to wait until the Politburo meeting at the end of July.