Industrial and Commercial Bank of China, Bank of China, China Construction Bank, Agricultural Bank of China, Bank of Communications, and Postal Savings Bank have all announced, heavyweight! Just now interest rate | deposit | Bank of China

A new round of deposit interest rate cuts is coming!

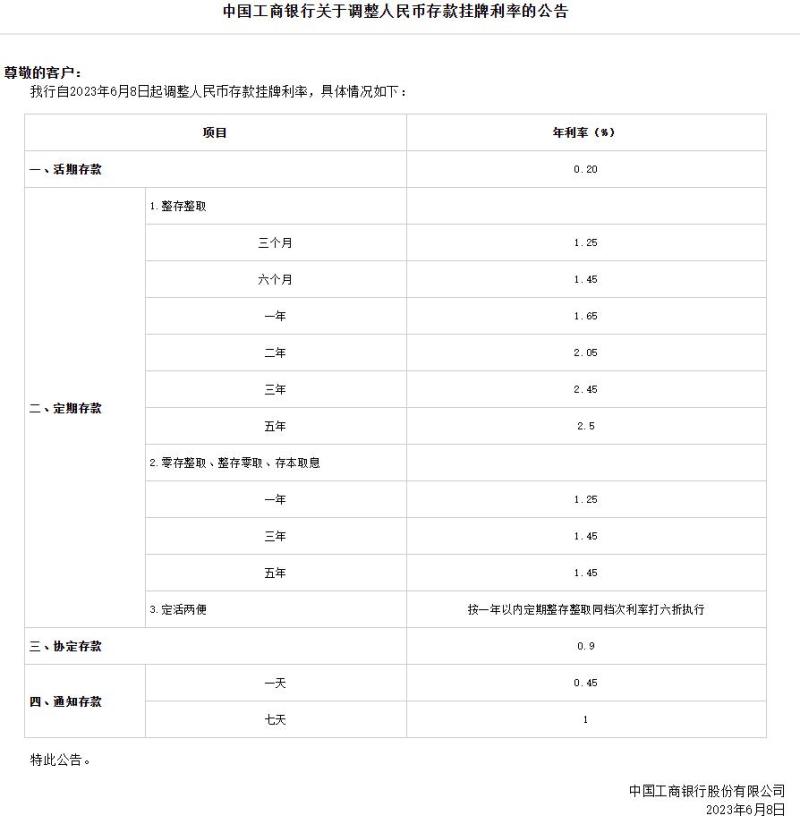

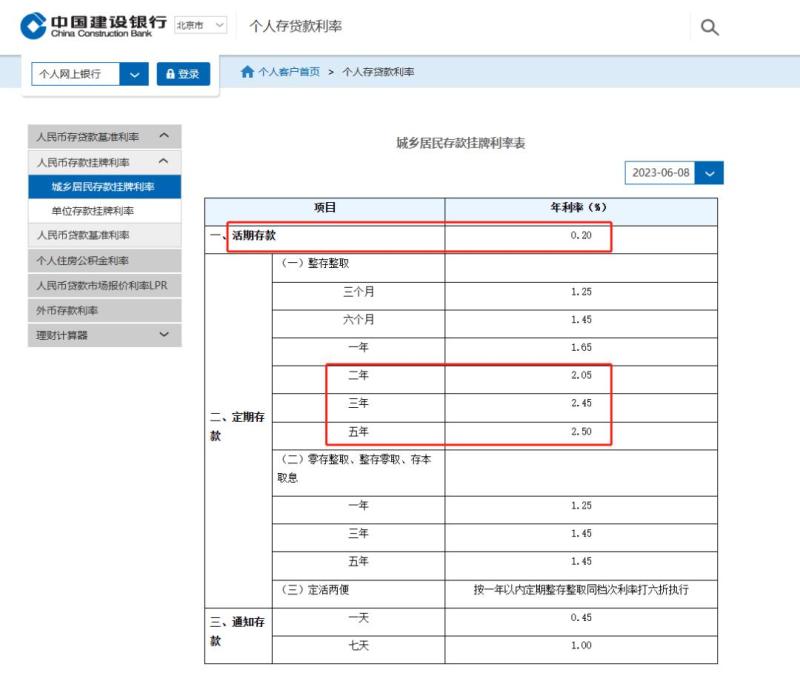

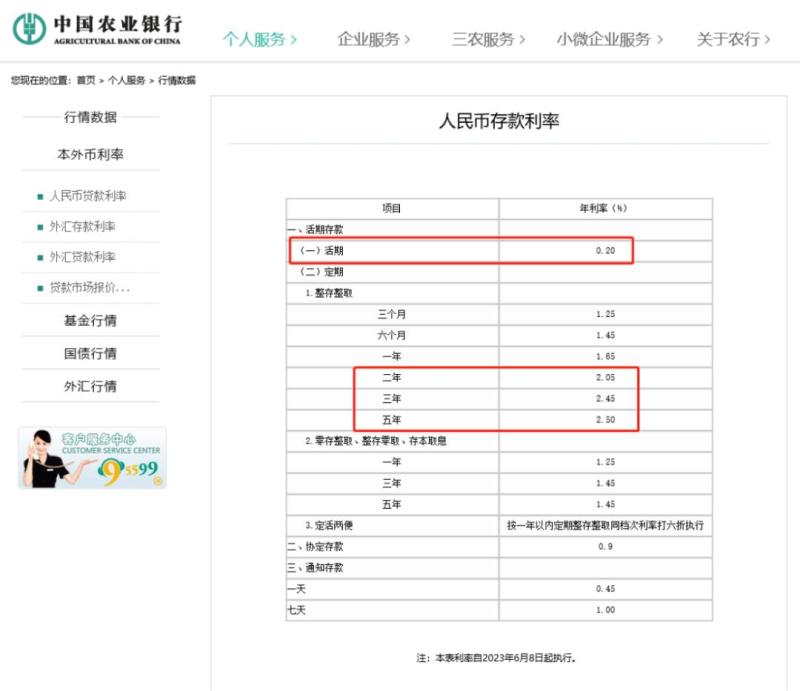

On June 8th, Industrial and Commercial Bank of China, Agricultural Bank of China, Construction Bank of China, Bank of Communications, and Postal Savings Bank of China jointly lowered their deposit listing interest rates.

Among them, the current deposit interest rate has been lowered from the previous 0.25% to 0.2%. The 2-year fixed deposit interest rate will be lowered by 10 basis points to 2.05%, the 3-year fixed deposit interest rate will be lowered by 15 basis points to 2.45%, and the 5-year fixed deposit interest rate will be lowered by 15 basis points to 2.5%.

In this round of adjustment, all listed interest rates have been lowered to below 2.5%, bidding farewell to the "three eras" of interest rates. However, the specific interest rates implemented by the same bank in different regions may vary slightly, and should be based on the local conditions. Due to restrictions on the upper limit of deposit interest rates, some products that banks can offer interest rate hikes will also be affected simultaneously.

This round of adjustment is just 9 months away from the previous round of adjustment. Last September, the six major banks collectively adjusted the interest rates of multiple products, including demand deposits and fixed deposits. Among them, the interest rates of 3-year fixed deposits and large deposit certificates were lowered by 15 basis points, the interest rates of one-year and 5-year fixed deposits were lowered by 10 basis points, and the interest rates of demand deposits were lowered by 0.5 basis points.

After the previous round of adjustment, the listed annual interest rate for current deposits in the six major banks was 0.25%; The listed interest rates for one-year, two-year, three-year, and five-year fixed deposits are 1.65%, 2.15%, 2.6%, and 2.65%, respectively. Stock banks, urban commercial banks, rural commercial banks, and rural banks have also gradually lowered their rates. In addition, the upper limit of interest rates for notice deposits and agreement deposits is also restricted, and some banks have lowered their interest rates by 55 basis points.

At the same time, according to multiple media reports, in this round of adjustment, US dollar fixed deposits have also been reduced according to different maturities and sizes. The interest rate for one-year US dollar fixed deposits above $50000 is not higher than 4.3%. Some banks have also adjusted their interest calculation methods, shifting the previous Libor based calculation model to a combination of listed interest rates and a floating rate.

Since the beginning of this year, the structure of bank deposits has continued to exhibit characteristics of being fixed term and long-term. According to central bank data, as of the end of April, the proportion of fixed-term and other deposits in personal deposits has risen to 71%, an increase of nearly 3 percentage points from the end of 2022; The proportion of fixed-term and other deposits in corporate deposits has increased by nearly 68%, an increase of nearly 2 percentage points from the end of 2022.

The team of Zhongtai Securities Bank believes that the simultaneous reduction of domestic and foreign currency deposit interest rates is due to both domestic and foreign factors. On the domestic side, multiple factors resonate, such as weak domestic consumption, pressure on bank interest rate spreads, and the continuation of the trend towards fixed deposits. In terms of overseas factors, on the one hand, the RMB deposit interest rate has been lowered multiple times, but the US dollar deposit interest rate continues to rise during the Federal Reserve's interest rate hike cycle.

Assuming that all banks in the market are implementing this adjustment, the RMB deposit reduction is expected to slow down by 3.17bp, and profits will increase by about 2.9%. State owned banks and rural commercial banks will benefit relatively more, with Chinese banks benefiting from a high proportion of current deposits and rural commercial banks benefiting from a high proportion of fixed-term deposits over a year. The reduction in US dollar deposit interest rates is expected to slow down by 0.6bp, and state-owned banks and joint-stock banks have a larger scale of US dollar deposits, benefiting relatively more.

After the major banks have lowered their prices, small and medium-sized banks may follow up to varying degrees, which can help alleviate the overall debt pressure on the industry. Although there are many types of downgrades involved this time, the magnitude is relatively small, and there is still room for a decrease in deposit interest rates.

The financial team of Huatai Securities pointed out in a research report that targeted reduction of domestic and foreign currency deposit interest rates can help reduce debt costs. Since 2022, the trend of deposit regularization has continued, and due to overseas interest rate hikes, foreign currency deposit interest rates have increased. Although the overall RMB deposit interest rates for various maturities have declined, the overall deposit interest payment rate has increased due to the impact of deposit regularization and foreign currency deposit pricing. This round aims to further improve the cost of bank liabilities by lowering deposit rates, especially fixed deposit rates, and guiding the reduction of bank USD deposit rates for the first time. Overall, the boost to bank performance is limited, and the signal significance is more worthy of attention.

In recent years, the regulatory authorities have further clarified the intention of cost reduction policies and continuously optimized the mechanisms. In June 2021, we will guide the transformation of the deposit interest rate pricing method. In April 2022, we will guide the deposit interest rate to be linked to 1Y-LPR+10Y treasury bond. In April this year, EPA introduced the deposit pricing penalty measures for the first time. Since April, the listing interest rates of some small and medium-sized banks and stock banks with higher pricing have been reduced successively; On May 10th, the national self-discipline mechanism lowered the self-discipline limits for contractual deposits and notice deposits, guiding a decrease in the cost of corporate current deposits.

The financial team of Huatai Securities stated that this cost reduction is aimed at bank current deposits, as well as high proportion fixed deposits and foreign currency deposits with higher pricing. It further guides the downward trend of deposit interest rates, which is conducive to maintaining the reasonable profit space of banks and enhancing their ability to supplement endogenous capital; In addition, guiding deposit interest rates downward is beneficial for promoting consumption and investment, and enhancing economic activity.