Expert interpretation: GDP grew by 6.3% year-on-year in the second quarter, overall | economy | GDP

Author | First Finance and Economics Wish Yan Ran

In the second quarter of 2022, China's economy only grew by 0.4% due to the impact of the epidemic. Under the influence of low base factors, GDP achieved a high growth of 6.3% in the second quarter of 2023.

According to data released by the National Bureau of Statistics on the 17th, preliminary calculations show that the gross domestic product (GDP) in the first half of the year was 59303.4 billion yuan, with a year-on-year increase of 5.5% at constant prices, which is 1.0 percentage point faster than the first quarter. From a quarterly perspective, the gross domestic product (GDP) increased by 4.5% year-on-year in the first quarter and 6.3% in the second quarter.

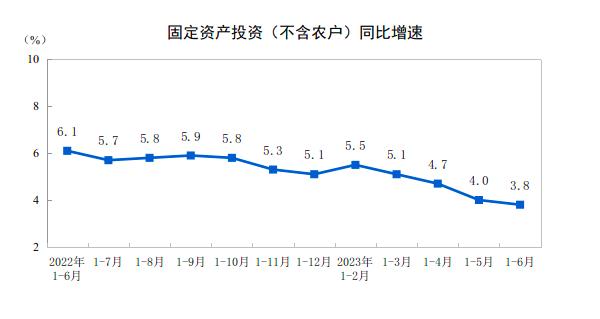

In terms of sub indicators, in June, the added value of industrial enterprises above designated size increased by 4.4% year-on-year, an increase of 0.9 percentage points compared to the previous month. The total retail sales of consumer goods reached 3995.1 billion yuan, a year-on-year increase of 3.1%, a decrease of 9.6 percentage points from the previous month. From January to June, the national fixed assets investment increased by 3.8% year on year, 0.2 percentage points lower than the previous month.

On the 17th, Fu Linghui, spokesperson for the National Bureau of Statistics, stated at the press conference of the State Council Information Office that overall, in the first half of the year, with the comprehensive restoration of normal economic and social operations, macroeconomic policies have shown significant effectiveness, and the national economy has rebounded and steadily advanced towards high-quality development. However, it should also be noted that the world political and economic situation is complex, and the foundation for sustained recovery and development of the domestic economy is still unstable. In the next stage, greater efforts should be made to transform the mode, adjust the structure, and increase the driving force, striving to promote the effective improvement of the economy in terms of quality and reasonable growth in terms of quantity.

The GDP growth rate of 6.3% in the second quarter was slightly lower than market expectations. Prior to the release of the data, multiple institutions predicted that the GDP growth rate in the second quarter would be around 7%. Economists participating in the Chief Research of First Financial Group predicted an average year-on-year GDP growth rate of 6.97% for the second quarter, while the Institute of Finance, Chinese Academy of Social Sciences, predicts a year-on-year GDP growth of 7%.

In terms of industry, downstream demand continued to be weak in June, with low prices of industrial products and overall industrial activity remaining weak. In June, the added value of industries above designated size increased by 4.4% year-on-year in actual terms.

Li Chao, Chief Economist of Zhejiang Securities, analyzed that the industrial production boom in June rebounded slightly month on month, but the intensity still needs to be strengthened. Profit pressure and destocking cycles still make industrial enterprises cautious about expanding production. Although the production of the service industry slightly declined in June, it still maintained a relatively high prosperity. The contact and new energy service industry maintained a positive trend, but the real estate sales prosperity was slightly insufficient.

According to a report released by the National Economic Research Center of Peking University, in June, due to the stabilization of domestic industrial economic demand, the operating rate of coking enterprises has rebounded, maintaining around 73%, and the operating rate of petroleum asphalt plants has rebounded to around 34%. The operating rates of all steel and semi steel tires are relatively stable, at 59.8% and 70.2%, respectively. The pressure on the growth rate of profits for industrial enterprises is still significant, and the destocking of domestic finished products is still ongoing. In the absence of a complete recovery in demand, enterprises will still prioritize destocking, and industrial enterprises still need to stabilize their expectations.

In terms of consumption, in the first half of the year, the total retail sales of consumer goods reached 2275.88 billion yuan, a year-on-year increase of 8.2%. Among them, the retail sales of consumer goods other than automobiles reached 20517.8 billion yuan, an increase of 8.3%. In June, the total retail sales of consumer goods reached 3995.1 billion yuan, a year-on-year increase of 3.1%.

Since the beginning of this year, as the economy and society have fully resumed normal operation, consumer promotion policies have continued to be strengthened. In addition, since May, the "May Day" holiday effect has significantly driven the recovery of service consumption in catering, culture, tourism, and other areas. Consumption of bulk commodities such as automobiles has continued to grow, and the overall consumer market in China continues to rebound and improve, gradually enhancing its driving effect on economic growth.

Wen Bin, Chief Economist of Minsheng Bank, stated that in June, the scene repair led to a return in consumer popularity and a compensatory recovery in service consumption. However, the consumer base is still unstable, and the speed of consumer recovery has slowed down.

From the perspective of main commodities, driven by the Dragon Boat Festival effect, the business activity index of transportation, accommodation, catering and other industries related to resident travel is still in the expansion range, but the expansion pace continues to slow down. The growth rate of automobile sales has significantly declined. From June 1st to 25th, the retail sales in the passenger car market decreased by 1% year-on-year, mainly due to the increase in the base caused by the car purchase tax reduction in June last year; The real estate market continues to cool down, housing prices in Baicheng continue to decline, and overall residential consumption related to real estate remains weak.

According to the analysis of Zhixin Investment Research Institute, in the second half of the year, multiple positive factors such as the arrival of the traditional consumption peak season, the stabilization of real estate sales and the improvement of automobile sales, as well as the increase in consumer promotion policies, will drive consumption to maintain rapid growth. In addition, with effective policy support, the employment situation may ease in the second half of the year, which will boost consumption. It is expected that consumption will increase by about 10% throughout the year.

In terms of investment, in the first half of the year, the national fixed assets investment was 24311.3 billion yuan, up 3.8% year on year. Among them, private fixed assets investment was 12857 billion yuan, down 0.2% year on year. On a month on month basis, fixed assets investment increased by 0.39% in June.

China International Capital Corporation (CICC) stated that real estate sales are still sluggish, especially for second-hand houses, where both quantity and price have seen a significant decline. The land market has only slightly rebounded, and the overall heat is still low. The physical workload at the infrastructure level is still weak, and the speed of housing construction has also slowed down. Against the backdrop of demand suppression, profit pressure, and the need to boost enterprise expectations, the manufacturing industry as a whole is weakening.

Industry insiders believe that since the second quarter, the Chinese economy has shown a recovery growth trend due to the combined effects of post epidemic recovery dividends, policy advancement, and low base effects. But with the further highlighting of issues such as weak endogenous driving force, insufficient effective demand, and unstable market expectations, the economic recovery momentum has slowed down. With the continuous efforts of macroeconomic policies to expand domestic demand and improve expectations, the endogenous driving force of economic recovery will gradually increase.

On July 6th, Premier Li Qiang presided over an expert symposium on the economic situation, stating that a comprehensive, dialectical, and long-term analysis and judgment of the current economic situation should be conducted, focusing on both generality and particularity, growth rate and structure and momentum, both domestic and global, as well as current and long-term trends. The long-term fundamentals of China's economy have not changed. As long as we maintain strategic determination and enhance development confidence, we are fully capable of promoting sustained and healthy economic development.

Regarding the economic trend in the second half of the year, Wang Qing, Chief Macro Analyst of Dongfang Jincheng, stated that with the implementation of policy interest rate cuts in June, regulatory authorities have once again emphasized the need to increase macroeconomic policy regulation. The next batch of new stable growth policies are expected to continue to be introduced. If the policies are implemented as scheduled, the economic recovery momentum is expected to strengthen in the third quarter, and the year-on-year GDP growth rate is expected to be around 5%, corresponding to a two-year average growth rate of 4.4%. In the fourth quarter, these two indicators are 6.0% and 4.4%, respectively.