Excavators are also affected, houses cannot be sold | year-on-year | excavators

The impact of the downturn in the real estate industry on the upstream industry chain is ongoing.

According to statistics from the China Construction Machinery Industry Association on major excavator manufacturing enterprises, in June 2023, sales of various types of excavators reached 15766 units, a year-on-year decrease of 24.1%. Among them, the decline in domestic sales was much greater than that of exports, with a year-on-year decrease of up to 44.7%. In the first half of this year, the sales of various types of excavators decreased by 24% year-on-year, with domestic sales decreasing by 44% year-on-year.

Excavators are the largest and most advanced product category in China's construction machinery market, occupying a core position. According to the sales data disclosed by the Construction Machinery Association in 2022, excavator sales reached 261000 units, which is higher than other types of construction machinery products and has the largest market size. Infrastructure and real estate are the main application areas of excavators.

In fact, excavator sales have shown a downward trend since mid-2021 and have continued to this day. According to the research report of Zhongtai Securities, the cumulative sales of excavators in 2022 decreased by more than 20% year-on-year, with the overall decline in domestic sales reaching 45%. The downward trend of bottoming out has not been significantly improved so far, and behind it is the sluggish demand for the two main downstream sectors of real estate and infrastructure.

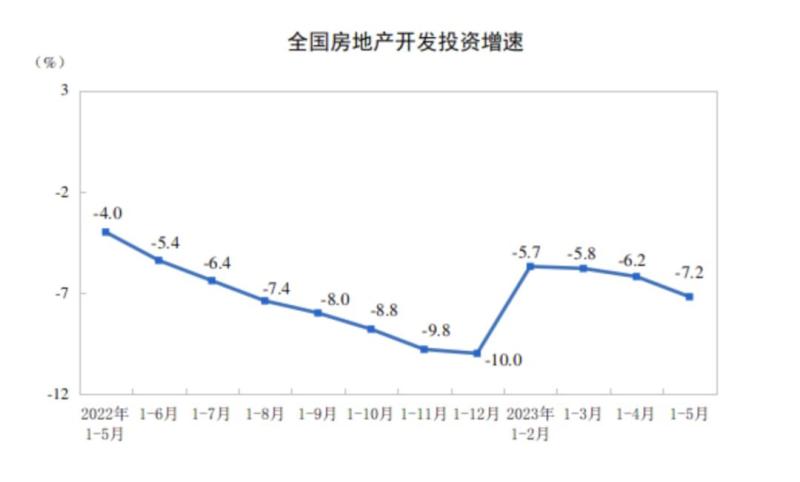

The real estate industry has entered a clear downward trend since the second half of 2021, with a continuous decline in investment intensity. According to data from the National Bureau of Statistics, since February 2021, the growth rate of real estate development investment in China has been continuously declining. By April 2022, the year-on-year growth rate had turned from positive to negative, and it still fluctuated and declined to this day.

According to the National Bureau of Statistics, in the first five months of this year, the newly started construction area of housing decreased by 22.6% year-on-year, an increase of 1.4 percentage points from January to April. Real estate development enterprises have a weak willingness to develop new projects; During the same period, driven by the "guaranteed delivery of buildings" policy, the completed area of houses increased by 19.6% year-on-year.

Due to the dual impact of a decrease in newly started construction area and an increase in completed construction area, the scale of ongoing construction of houses has decreased. From January to May, the construction area of houses decreased by 6.2% year-on-year, with an expanded decline compared to the previous four months. Overall, from January to May, real estate development investment decreased by 7.2% year-on-year, an increase of 1 percentage point from January to April.

Yan Yuejin, the research director of E-House Research Institute, analyzed that in the first five months of this year, the investment in real estate development decreased by more than 7% year-on-year, indicating an overall deterioration and a lack of motivation to boost. The current weak expansion capacity of real estate companies on the supply side is related to the lack of good absorption of existing policies and the lack of significant boost in sales data. In addition, from the perspective of real estate and the real economy, the development investment data is weak, which will have a greater impact on fixed assets investment and industrial chain around the country.

One of the key reasons for the insufficient willingness of real estate companies to start construction is the sluggish sales. As early as the end of 2021, a senior executive from a real estate company mentioned that a project involves several buildings starting construction at the same time, with a large scale of project payments. If the construction progress is accelerated but sales cannot keep up, there will be situations where there is no funds to pay for the project payments, so poorly sold projects will be suspended. Correspondingly, projects that sell well or have already been sold out will accelerate construction. Many insured real estate companies also emphasize the need to preserve liquidity to ensure "insurance delivery" work.

Since 2023, the real estate market has experienced a significant rebound in February and March, but with the release of previously suppressed housing demand coming to an end, the market has rapidly cooled since April. In June, when real estate companies were supposed to sprint for semi annual performance, they used to increase their supply to boost sales, but this year they have clearly lacked enthusiasm. According to a research report by Guoxin Securities, the supply volume of real estate companies in June this year hit a new low in the same period in nearly five years.

The insufficient supply also limits the sales performance of real estate companies. According to the sales data released by Kerui, in June this year, the comprehensive sales revenue of the top 100 real estate companies was 601.5 billion yuan, with a month on month growth rate of only 9.5%, lower than the performance of the same period in history; Compared to the same period last year, there was a decrease of 27.6%. Overall, the cumulative full caliber sales of the top 100 real estate companies in the first half of this year decreased by 0.4% year-on-year, indicating weak momentum for the recovery of the real estate market.

Poor sales and insufficient funds further suppress the land acquisition efforts of real estate companies. According to the list of the top 100 real estate companies in terms of land acquisition released by China Index Research Institute, in the first half of this year, the cumulative total land acquisition amount of the top 100 real estate companies was 592 billion yuan, a year-on-year decrease of over 10%, and the decline rate expanded by nearly 2 percentage points in the first five months. The Zhongzhi Institute predicts that in the short term, despite no significant improvement in sales receipts and financing, real estate companies will still face significant challenges in cash flow, directly restricting their enthusiasm for starting construction and investment. It is difficult to see a significant improvement in the amount of investment in new construction and real estate development.

It is worth mentioning that besides real estate, there is another major source of demand for excavators, which is the infrastructure industry. According to a research report from Zhongtai Securities, since 2022, in the context of the continuous downturn in the real estate industry, infrastructure investment has played a role in supporting and stabilizing the growth of the excavator industry. There have been differences in the trend of new construction area and excavator sales indicators, and the growth rate of infrastructure investment and excavator sales is relatively consistent.

However, the growth of infrastructure investment has also shown signs of weakness recently, showing a monthly downward trend since April. According to data from the National Bureau of Statistics, infrastructure investment increased by 8.8% year-on-year from January to March this year. The year-on-year growth rate from January to April fell to 8.5%, and the growth rate from January to May further decreased by 1 percentage point to 7.5%.

This trend may be improved. In a research report in late May, CITIC Securities pointed out that the operating rate of excavators in most provinces across the country has gradually improved. In the future, with the large-scale investment of social financing, infrastructure construction is expected to gradually accelerate, and downstream demand in the construction machinery industry is expected to continue to improve.