Central important deployment! The real estate industry is transitioning smoothly towards a new development model | real estate | model

The Political Bureau of the Central Committee of the Communist Party of China held a meeting on July 24th to analyze and study the current economic situation and deploy economic work for the second half of the year. The meeting pointed out that timely adjustment and optimization of real estate policies should be carried out, and the policy toolbox should be well utilized to better meet the rigid and improved housing needs of residents, promoting the stable and healthy development of the real estate market.

In recent years, the Party Central Committee has repeatedly proposed new development models for the real estate industry. The real estate market is experiencing positive changes, but there are also hidden concerns. What are the main problems currently facing the real estate industry? How to smoothly transition to the new development model? Recommend the latest article from the People's Forum.

Why propose a new development model for the real estate industry?

In December 2021, the Central Economic Work Conference first proposed "exploring new development models" regarding the development of the real estate industry; In December 2022, the Central Economic Work Conference pointed out that "eliminating the drawbacks of the 'high debt, high leverage, and high turnover' development model over the years, and promoting the smooth transition of the real estate industry to a new development model." In recent years, the reason why the Party Central Committee has repeatedly proposed a new development model for the real estate industry is mainly related to the following four aspects.

Firstly, it is related to the significant decline in the real estate market since 2021, an increase in corporate defaults, and the emergence of unfinished projects. According to data released by the National Bureau of Statistics, the real estate market has experienced a significant decline for over 20 months since the second half of 2021. In 2022, the year-on-year growth rates of sales area and sales revenue of commercial housing for the whole year were -24.3% and -26.7%, respectively. The year-on-year growth rates of land purchase area and new construction area of housing were -53.4% and -39.4%, respectively; At the same time, according to Wind data statistics, from 2021 to 2022, the balance of domestic debt default day bonds and the number of extended bonds of Chinese real estate enterprises increased from 21 billion yuan and 15 to 188.4 billion yuan and 114 respectively; In 2022, there were also some suspended and unfinished projects. In order to solidly carry out the work of guaranteeing the delivery of buildings and promote the stable operation of the real estate market, on March 3, 2023, Pan Gongsheng, then Vice President of the People's Bank of China, pointed out in response to a reporter's question: "We have launched a special loan for guaranteeing the delivery of buildings of 350 billion yuan, established a support plan for guaranteeing the delivery of buildings of 200 billion yuan, and a support plan for leasing housing loans of 100 billion yuan." It can be seen that the real estate market has experienced a significant and prolonged decline, which has also exposed some problems. It is urgent to consider whether the past development model of the real estate industry can be sustained.

Secondly, it is related to the failure of regulatory cycles. In the past, the real estate market has also experienced negative growth in sales area and sales of commercial housing in years such as 2008 and 2014. But at that time, as long as the regulatory policies were relaxed, the market would immediately rebound. In this market downturn, the government began to change financial policies in October 2021. In 2022, local governments introduced more than 300 policies to relax regulation. The mortgage loan interest rate for home purchases has dropped to a historical low, but the market is still hovering at the bottom. The effect of policy relaxation is far less than before. It is necessary to study the new trends and structural changes in the real estate industry.

Again, it is related to implementing the new development concept. The requirements put forward by the Party Central Committee in recent years regarding high-quality development, meeting the people's aspirations for a better life, and implementing the new development concept need to be implemented in the process of developing the real estate industry. In December 2016, after the Central Economic Work Conference first proposed the positioning of "housing for living, not for speculation", the government insisted on improving the "two systems" of housing security and housing market, and through measures such as stabilizing land prices, housing prices, and expectations, promoted housing to return to its livelihood attributes. Preventing industry risks and promoting balanced development between the real estate industry and the real economy need to be reflected in the new development model of the real estate industry.

Finally, it is related to the new stage of development that our country is in. The rapid growth of China's real estate market in the past relied on four major dividends: first, the policy dividend of releasing market demand brought about by the cessation of welfare housing distribution; second, the dividend of population and urbanization; third, the monetary dividend of abundant liquidity; and fourth, the dividend of high-speed economic growth. After more than 20 years of development, the task of compensating urban housing arrears has been basically completed. In 2020, the per capita housing construction area in China's urban areas has reached 38.6 square meters; The proportion of working age population has been declining since 2012, and the average annual increase in urban permanent residents has decreased from over 20 million before 2018 to 6.46 million in 2022; China's economic development has entered a new normal, and the development of the real estate industry needs to adapt to the characteristics of the new era.

The new development model of the real estate industry needs to adhere to a problem oriented approach

Studying the new development model of the real estate industry requires taking the old development model as the anchor point, analyzing the problems existing in the old development model, and proposing solutions to improve the problems of the old development model. Only in this way can the proposed new development model of the real estate industry be meaningful. The current problems in the real estate industry mainly include the following aspects.

Firstly, the single land supply model still needs to be optimized.

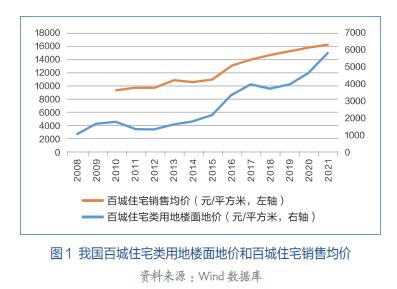

At present, urban governments are still the absolute mainstay of real estate land supply in China. The single source of land supply continuously drives up land prices, further increasing the risk of rising housing prices and market fluctuations. In terms of land supply prices, the "bidding, auction, and hanging" transfer method of "the higher the price, the better" creates conditions for the increase in land prices. Under the "bidding, auction, and hanging" transfer method of "the higher the price, the price of residential land continues to rise, and the rapid rise in housing prices is closely related to this. According to Wind database data, in 2020, among the 22 key cities, Beijing, Hangzhou, Chengdu, Ningbo, and Xiamen had a ratio of 76%, 52%, 59%, 56%, and 53% of floor to residential sales prices, respectively. Between 2010 and 2021, the floor price of residential land in Baicheng increased by 2.3 times, while the average residential sales price only increased by 0.7 times during the same period, with land prices rising more than housing prices.

In terms of land supply scale, there is an imbalance in the linkage between people, land, and housing. Some hot cities have insufficient land supply, which has pushed up land and housing prices. At the same time, some cities have excessive supply, resulting in excessive inventory. According to statistics from scholars, since 2003, more and more construction land supply in China has been allocated to the central and western regions. By 2014, the proportion of land supply in the central and western regions of China has approached 60%, and the proportion of construction land supply has increased by 30 percentage points; According to the National Land Use Master Plan Outline, 65% of the newly added construction land will be allocated to the central and western regions by 2020. During the same period, the population in the eastern region increased by nearly 50 million more than that in the central and western regions, indicating that the mismatch of land supply indicators has exacerbated the contradiction between supply and demand in the real estate market in the eastern region, especially in large cities with net population inflows.

Secondly, the "four heavy and four light" housing supply model is unbalanced.

One is to prioritize sales over renting. In recent years, housing prices in many cities in China have skyrocketed, significantly exceeding the increase in income and rent, leading to expectations of sustained price increases. This has led to panic among some urban residents who enter the market, consume in advance, and purchase houses with high leverage, suppressing the normal demand in the rental housing market. In addition, the different rental and purchase rights in areas such as children's education and residence permit application have forced some tenants to choose to purchase a house in advance. The reason for this is that the housing policy has long emphasized buying and selling over leasing, neglecting the cultivation and management of the housing rental market, and unable to adapt to the direction of the housing system reform that combines renting and purchasing in recent years.

The second is to rejuvenate the old. The insufficient attention and support given by China's housing policy to the maintenance and upkeep of old residential buildings have limited the improvement of housing quality. The special maintenance fund for residential buildings is an important fund for the maintenance of affordable housing in China, mainly used for the maintenance and renovation of shared areas and facilities after the warranty period expires. However, with the increase of elderly residential buildings, there is a significant gap between the actual collection and demand of special maintenance funds for residential buildings, and there are also many problems in their use and management. This not only directly affects the safe use of commercial housing throughout its entire lifecycle, but also involves the preservation and appreciation of housing assets of urban households, directly affecting the improvement of housing satisfaction among urban residents.

The third is to prioritize the market over security. From the perspective of the housing security system, the multi-channel guarantee mechanism is not yet perfect. On the one hand, the coverage of housing security is relatively narrow, and a considerable number of cities have not included "new citizens" in the housing security system. The monetary subsidy housing assistance policy still needs to be improved. On the other hand, in policy design, rental based security is the main approach, and the issue of children's education has not been effectively resolved, making it difficult to meet the housing needs of the urban "sandwich layer" group. At the same time, the allocation of housing security is unreasonable. According to the sixth and seventh national population censuses, the proportion of newly built affordable housing units in towns to the number of newly added households in the past 10 years was 10%, higher than the 8% level in cities, and towns are precisely the most suitable place for monetary subsidies.

The fourth is to prioritize pre-sale over ready-made houses. The pre-sale system has multiple drawbacks, leading to some risks and hidden dangers. China implements a pre-sale system for commercial housing, where buyers have directly paid the full purchase price to the development enterprise before the house is built and delivered. According to data released by the National Bureau of Statistics, since 2009, the proportion of mid-term housing sales in China has consistently exceeded 75%. Among them, in 2019, 2020, and 2021, it reached 87.9%, 89.8%, and 89.6%, respectively. Under the current pre-sale system, homebuyers almost bear all the risks of unfinished and low-quality properties, while pre-sale funds have become an important interest free lever for development enterprises, greatly reducing the entry threshold for real estate development. It was not until the government introduced the "guaranteed delivery" measures in 2022 that the problem was controlled.

Thirdly, the development model supported by high housing prices is difficult to sustain.

In the past, real estate development enterprises adopted a "high debt, high leverage, and high turnover" real estate development model. "High debt" is reflected in the fact that the asset liability ratio of domestic listed real estate companies is generally above 80%, with many real estate companies exceeding 100%, far higher than the debt level of the manufacturing industry. According to the Wind database, the asset liability ratio of listed real estate companies in China reached 79.4% in 2021, second only to the financial industry. From the perspective of the growth rate of asset liability ratio, the real estate industry ranks first. From 2010 to 2021, the asset liability ratio of the real estate industry increased by 12.7 percentage points, more than twice that of the second ranked energy industry.

"High leverage" is manifested in real estate development, which includes not only financial leverage but also operational and cooperative leverage, and is unique to real estate development enterprises. The operational leverage mainly includes two aspects: first, upstream and downstream enterprises advance funds. For example, in 2022, various types of accounts payable accounted for 31.2% of the sources of real estate development investment funds, far higher than the proportion of domestic loans of 11.7%; The second is to use pre-sale deposits, down payments, and mortgage loans to obtain new projects. In 2022, pre-sale deposits and mortgage loans accounted for 49% of the development investment funds. Collaborative leverage mainly refers to the rapid expansion of scale with small investment through enterprise cooperation and development, striving for consolidation. Figure 3 shows the trend of cooperation leverage among real estate development enterprises, with larger scale real estate enterprises having relatively larger cooperation leverage.

"High turnover" is reflected in the fact that real estate enterprises mainly rely on fast selling commercial housing to achieve profits. In 2021, among the main business revenue of real estate development enterprises, the sales revenue of commercial housing accounted for 94.9%. Supported by increased leverage, the three-year compound sales growth rate of China's top 30 real estate companies from 2016 to 2018 reached a median growth rate of 40%. Due to the concentration of funds and land resources towards large-scale real estate enterprises, over the years, real estate enterprises have tasted the sweetness of increasing leverage and boosting scale, and scale first has become an industry consensus. However, leveraging and operating with high debt is a double-edged sword for real estate companies, and the "three highs" model requires sustained support from rising "high housing prices". Under the positioning of "housing for living, not for speculation" and with the reduction of dividends from the rapid growth of the industry, the space for housing price increase is under control, high returns are no longer available, high turnover fails, and the risk of high leverage becomes more prominent. The "three highs" real estate development and operation model is difficult to sustain.

Fourthly, the financing model of real estate enterprises mainly based on debt faces high risks.

Compared with developed economies, China's real estate enterprises have a significant proportion of indirect financing and a higher debt financing ratio. In 2021, the asset liability ratio of listed real estate companies in China's real estate industry reached 79.4%. In comparison, the average asset liability ratio of the four leading real estate companies in Hong Kong in 2018 was only 32%. Among them, the asset liability ratios of New World Development, Changshi Group, Henderson Land, and Sun Hung Kai Properties were 47%, 28%, 28%, and 23%, respectively. The debt ratio of real estate companies in other countries is also much lower than that in China, such as 57% in the United States and 38% in the United Kingdom. In the development process, Chinese real estate companies rely on trust funds, development loans, and other methods for financing. As project uncertainty decreases, they continuously replace high cost financing with low-cost financing. For example, after obtaining the pre-sale certificate, they can use low-cost development loans to replace high cost trust funds. Real estate companies also increase off balance sheet liabilities through upstream and downstream loans, and require construction companies to advance funds; In the sales process, the pre-sale system has become a tool for real estate companies to leverage, but under the pre-sale system, buyers may not have sufficient understanding of the risks they need to bear. When housing prices no longer rise, sales turnover speed decreases, and financing pressure increases, the debt risk of real estate companies will continue to accumulate and manifest, and spill over to upstream and downstream enterprises and homebuyers.

Fifth, the operational model of commercial real estate is not mature enough.

China's commercial and operational real estate holdings lack long-term financial support, mainly through retail sales. The management level still needs to be improved, and in recent years, inventory has continued to rise, leading to a higher vacancy rate. In 2020, the new construction of commercial real estate in China reached 600 million square meters, an increase of 75% compared to 2010, higher than the 27% increase in newly started housing area during the same period. Due to factors such as economic cycles and changes in industrial structure, the demand for commercial properties in traditional industries has decreased. Long term oversupply has led to a continuous increase in the unsold area of commercial real estate and a rising vacancy rate. According to Cushman&Wakefield data, in June 2021, the vacancy rates of Grade A office buildings in Beijing, Shanghai and Shenzhen will be 17.5%, 14.6% and 22.3% respectively. The operational efficiency of a large number of existing commercial real estate in our country is not high, and a mature operational model has not yet been formed. Compared to developed economies, the highest market value real estate companies are often not development companies, but leasing real estate investment trusts, comprehensive service companies, asset management companies, etc. This is worth referring to for the transformation and upgrading of domestic real estate enterprises.

The direction of new development models in the real estate industry

"Housing is for living, not for speculation" is the fundamental requirement of the new development model of the real estate industry, high-quality development is the main goal of the new development model of the real estate industry, and stable diversification is the specific embodiment of the new development model of the real estate industry. The key lies in promoting the establishment of a new development model for the real estate industry, designing new systems, promoting supply side structural reform of the real estate industry, and achieving high-quality supply that matches demand.

Firstly, transform from "only" to "one" and promote the reform of diversified supply models for real estate land.

Diversified supply of real estate land will help reduce land costs and force local governments to reduce or even break free from their dependence on land finance. From an economic perspective, the continuous rise in land and housing prices is rooted in the mismatch between insufficient supply and strong demand. The current real estate land supply model characterized by "bidding, auction, and hanging" has a significant impact on the formation of the real estate market pattern. It is not only the source of problems such as pushing up housing prices, forming mismatches, and eroding corporate profits, but also a strong support for China's urbanization infrastructure construction. The core of future reform is to seek benefits and avoid harm, changing the "bidding, auction, and hanging" land supply method from "only" to "one", and promoting the formation of diversified channels for land supply.

One is to build a unified land market for urban and rural areas. Summarize the experience of constructing affordable rental housing on rural collective construction land, promote the entry of rural collective construction land and homestead land into the market in a timely and planned manner, expand the supply channels of real estate development land, build a fully effective new competitive pattern in the primary land market, and force local governments to reduce their dependence on land finance, actively support industrial development to obtain taxes, and divert the housing market demand of some large cities with excessive pressure.

The second is to activate the existing construction land through market-oriented mechanisms. Activate the secondary land market and explore the implementation of a flexible land use change system within the stock renewal area, such as allowing for timely adjustment of commercial and office land or housing use that clearly does not meet market demand or is idle and vacant to residential use; Allowing a certain proportion of land use flexibility within industrial zones to promote industrial upgrading and balance between work and housing. Implement urban renewal actions, organize the preparation of special plans for urban renewal areas, and invest existing land resources into higher output areas through multiple channels.

The third is to establish a market-oriented land transaction mechanism based on "supply determined by people". According to the principle of coordinating urban housing supply with population growth, adjust the allocation basis of annual indicators for urban construction land, and dynamically adjust residential land indicators based on changes in permanent population; By utilizing a cross regional trading mechanism for national construction land and supplementary arable land indicators, we aim to achieve a cross regional balance of land use indicators from within the province to across the country, form an advantage in industrial agglomeration, and improve land use efficiency and overall economic output.

The fourth is to innovate and introduce policies for the continuation of land use rights after they expire. The urban functions need to be continuously improved, but to prevent large-scale demolition and construction, it is necessary to preserve the urban memory, continue the urban style, and formulate and implement policies for the continuation of residential, commercial, and industrial land use after the expiration of their term. Considering the need for urban industrial structure adjustment, it is recommended to implement a "new lease+annual land lease system" for commercial and industrial land, to solve the problem of social capital being unable to invest in existing buildings that urgently need to be updated due to the short land use period, accelerate urban industrial upgrading and functional improvement, and smoothly connect the changes in the use period, purpose, and plot ratio of new and old buildings.

Secondly, with "affordability" as the core, we will promote the reform of the diversified housing supply model.

The period of absolute shortage of housing in China has passed, and high housing prices are the main problem at present. At this stage of development, the focus of housing management needs to shift from the demand side to the supply side, fully considering the regional structural differences in housing demand, as well as the "four heavy and four light" problems in housing supply, promoting diversified housing supply, and achieving "affordable rental and purchase".

One is to standardize and promote the development of housing leasing. Implement the Opinions on Accelerating the Development of Affordable Rental Housing issued by the General Office of the State Council, and increase the supply of rental housing through multiple channels. Ensure equal rights for renting and selling, and effectively solve the problem of tenants enjoying equal access to public services such as education and medical care. Without the implementation of equal rights for rent and purchase, rental housing can only be a transitional and temporary demand, and cannot become the norm.

The second is to increase the guarantee of property rights based housing. Property based housing security is another effective way to improve the affordability of housing. The rise in housing prices is related to the improvement of total factor productivity, therefore, the pressure of rising housing prices in big cities will continue to exist, and housing security is a long-term task. Rental and property rights protection are both important forms of protection. Shared property rights housing can build a bridge between rental housing and market commodity housing, forming a complete tiered affordable housing supply system to meet the differentiated housing needs of different income groups at different stages of life. Shared ownership housing has been successfully practiced in the UK, the United States, and Beijing, Shanghai, and other places in China. In the future, increasing the supply of shared property housing in major cities in China can achieve a win-win situation. If it can reduce the expenses of homebuyers and solve the problem of insufficient housing affordability in big cities; Can alleviate the financial pressure on the government to build affordable rental housing; The government can recover the transferred benefits when selling the remaining property rights in the future, and the housing security resources can be recycled; It is an important tool to expand the middle-income group by enabling young people to realize their dream of moving from renting to owning property rights housing; It can become a talent incentive method, and rewards based on the proportion of shared property rights are more conducive to retaining talents; When the housing market fluctuates, the government can guide demand and stabilize housing investment by expanding or reducing its own property rights ratio.

The third is to support the upgrading and improvement of housing. In the long run, people's yearning for a better life, including the continuous improvement of housing conditions, is an inevitable housing consumption model of "rent before buy, small before big, old before new". Effective release of demand for improved housing can be achieved through measures such as lowering the entry threshold for improved housing, increasing the optimization of tax policies, and supporting the supply of elderly housing, making the demand for improved housing a key factor in stabilizing the real estate market.

The fourth is to reform the current pre-sale system of commercial housing into a purchase order system. To protect consumer rights and respect the general laws of commercial housing sales, China can learn from international experience and change the development mechanism of pre-sale funds as interest free leverage for real estate enterprises. Measures such as collecting deposits through pre-sale or increasing the proportion of currently sold residential properties can reduce the risks of homebuyers, improve the stability of industry development and the quality of residential products.

The fifth is to innovate the renewal model of existing housing. Explore the mechanism for supplementing special maintenance funds for residential buildings. In addition to paying special maintenance funds for new houses when purchasing, a certain proportion of fees need to be collected during second-hand house transactions, or a certain proportion of funds need to be allocated from the value-added tax levied on real estate transactions, and recycled to the special maintenance funds for houses in the community; Exploring the independent renewal mode of old residential communities, with special maintenance funds for residential communities, we can innovate the independent renewal mode of old residential communities, establish a pre consultation mechanism for renewal and renovation, respect the status of residents as the main body, and with government support, mainly rely on the power of the community itself to achieve the renewal and quality improvement of old residential communities; Improve the level of intelligent property management services, encourage property service enterprises to provide extended services such as elderly care, childcare, and housekeeping, explore the "property service+life service" model, improve the supporting facilities around residential areas, and continuously improve the convenience of life.

Once again, the diversification of stocks and bonds promotes the reform of financing models in the real estate industry.

In the future, the reform direction of the financing model in China's real estate industry needs to shift from mainly relying on debt financing in the past to "diversified stock and debt". Specific policies need to have both obstacles and shortcomings. While maintaining the direction of debt reduction, we should broaden the channels for equity financing for real estate enterprises and increase the proportion of direct financing.

One is to promote the operation of bulk property public REITs. Incorporate real estate companies' holdings of operational properties, such as apartments, commercial buildings, office buildings, hotels, etc., into the operation of public REITs. Utilize public REITs to combine the overall operation and liquidity of bulk properties, effectively activate existing assets, and strengthen the support of the capital market for the flow of real estate property rights. The second is to facilitate financing channels in the capital market. Implement the opening of A-share financing channels for real estate enterprises, strengthen the ability of the capital market to serve the real economy, and use the power of the market to resolve risks. Thirdly, we will vigorously develop private equity funds. Support the acquisition of real estate assets by "holding type" real estate private equity funds, open up exit channels, strengthen coordination with bulk property public REITs, and effectively reduce the leverage of real estate enterprises. The fourth is to strictly regulate the financing of real estate enterprises. Strictly control the illegal self financing of real estate enterprises, innovate the supervision methods of non debt financing of real estate enterprises, standardize the signing of investment, procurement, and construction contracts of real estate enterprises, clarify the constraints of "explicit equity and real debt", "supply chain financing", and "commercial bill financing", and avoid "hidden leverage". The "Three Arrows" policy for real estate financing introduced by relevant departments in December 2022 is not only an important policy tool for resolving real estate market risks, but also an important policy to support the transformation of the real estate industry towards a new development model.

Finally, promote the reform of real estate enterprise business models through profit diversification.

In the current and future period, China's real estate industry will transition from a "growth period" to a "mature period". The transformation of the business model of real estate enterprises is mainly reflected in the diversification of profit sources. Correspondingly, it requires the development model of real estate enterprises to transform from "high debt, high leverage, and high turnover" to an integrated development, operation, and service that emphasizes both light and heavy aspects; The financing model of real estate enterprises is transitioning from high debt to diversified equity; The target model of real estate companies is shifting from pursuing scale expansion and high speed to brand and quality improvement.

The changes in external environment and policy traction have changed the development logic of the industry. Real estate companies need to shift from extensive expansion to refined operation, from relying on external dividends to enhancing competitive advantages through refined management to obtain dividends, and change the profit and income structure of real estate enterprises. One is to tap into internal management dividends. In the future, real estate companies will have more restrained and focused investments, more precise and efficient sales, more humanized and cost reducing designs, more controllable and excellent engineering, and more intelligent and diversified property management. The second is to attach importance to strategic leadership. When the real estate industry is transitioning from high-speed growth to high-quality development, real estate companies need to formulate new development strategies based on "reasonable growth rate, profit orientation, and risk control". The third is to strengthen organizational and standardized guarantees. Real estate companies need to establish new capabilities that match strategic dynamic adjustments and changes in development models. The transformation of organizational functions around the construction of efficient organizations requires a shift from control to support, from supervision to motivation, and from command to empowerment. On machine