After rising by over 20% this year, global funds may temporarily stop flowing into the Japanese stock market. Data | Japan | Global

Since the beginning of this year, the Japanese stock market has blossomed with iron trees, attracting global capital inflows. Chinese retail investors have maintained a high level of enthusiasm for subscribing to Nikkei ETFs. However, after both the TOPIX index and the Nikkei 225 index recorded over 20% growth this year, many international institutions have indicated that market volatility will intensify and the upward trend may temporarily pause.

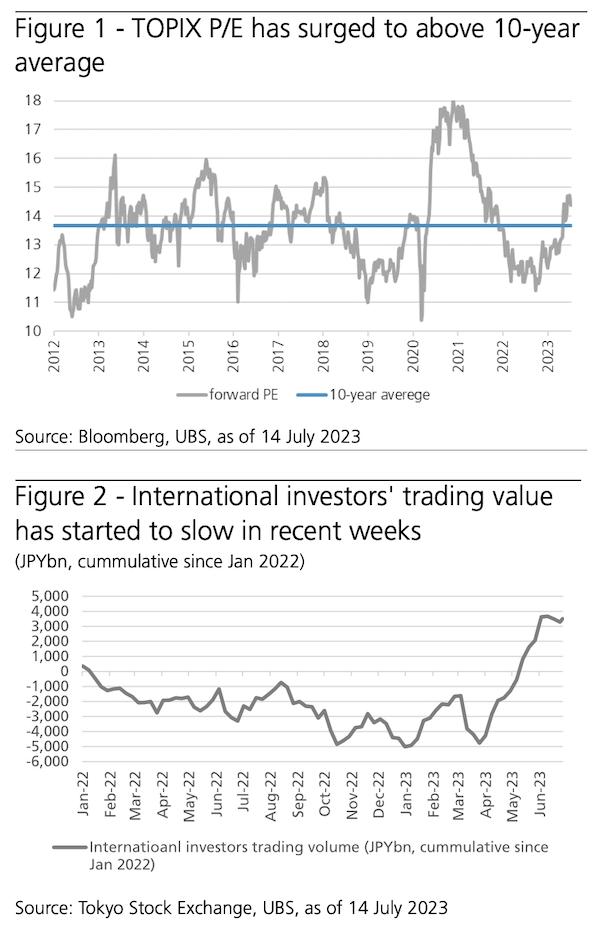

UBS's CIO office told reporters that the valuation of the Japanese stock market is no longer cheap compared to historical averages. Although it is still attractive compared to the S&P 500 index, this gap has narrowed; International investors may establish positions in Japanese stocks starting from the extremely low point in 2022. Recent weekly data shows that the net trading value of foreign investors has begun to slow down; During the financial reporting season starting in summer or June, the number of Japanese stock repurchases may decrease; Furthermore, as US interest rates approach their peak, further depreciation of the yen is unlikely to occur.

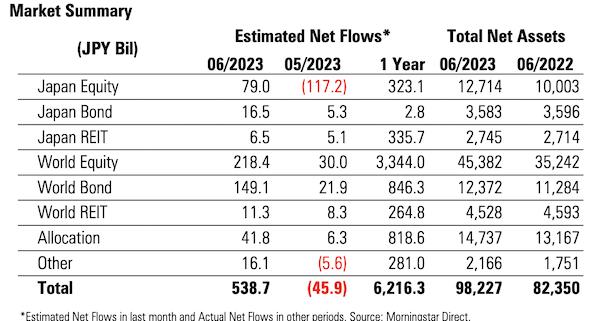

Global capital increase in Japan

According to data from Morningstar, the net inflow of funds from global funds into Japanese assets rebounded to 540 billion yen, making it the second highest month of the year, while May saw a net outflow of 50 billion yen. June was also the first time in nine months that all categories had net inflows - stocks, bonds, and allocation categories all performed strongly. Among them, Japanese stocks saw a net inflow of 80 billion yen from a net outflow of 120 billion yen in May.

The rebound in inflation, wage increases, and the expected improvement in corporate investment returns are all reasons driving the increase in foreign investment. Rob Subbaraman, head of global macro research at Nomura, previously stated in an interview with First Financial that he is still optimistic about the prospects of the Japanese economy and stock market. "Deflation has plagued Japan for 20 years, but it has finally rebounded in the past year. At the same time, due to labor shortages, Japanese women are encouraged to participate more in the labor market, especially middle-aged women, which is a positive change."

Many institutions believe that when wages rise and there is no surplus labor in the market, it means that employees have stronger premium ability, which can increase their mobility and seek higher wages, making labor distribution more effective and improving productivity. At the same time, this will also encourage companies to invest in more labor-saving technologies and help improve productivity. In addition, Japanese households keep half of their savings in banks, and their savings are still at negative interest rates. The current situation will prompt them to consider moving their savings, such as investing in the stock market, which will give the stock market better upward mobility.

"There have also been positive developments in corporate governance, with the Tokyo Stock Exchange putting pressure on companies with low PB to improve their balance sheets, better utilize cash, increase returns and dividends," said Nomura. This is also one of the main reasons why global funds are increasing in Japan.

Data shows that Japan's nominal wage growth in recent months is reflected in the results of the spring 2023 wage negotiations, with a year-on-year increase of 3.6%. The nominal salary in May increased by 2.5% year-on-year; The core CPI reached 4% in the first quarter of 2023. Although institutions expect the medium-term core CPI to slow down to 1% to 1.5%, this is still much higher than the average level of 0.3% in recent decades.

In addition, facing rising inflation, the central bank has no intention of raising interest rates, and the yen remains weak, which also helps the stock market. "There are speculations that the Bank of Japan may further adjust its yield curve control policy at next week's meeting. However, Bank of Japan Governor Kazuo Ueda stated that this is not the case, indicating that the YCC will not change in the end. Regardless, the Bank of Japan's ultra loose monetary policy will continue to accompany us for a long time." Jerry Chen, senior analyst at Kasei Group, told reporters that after decades of structural deflation, the Bank of Japan will not act too hastily at present.

It is worth mentioning that the Japanese stock market has not only been booming globally, but has also attracted the attention of Chinese retail investors since May. It has also led to a significant premium for the Nikkei 225 ETF at one point. For example, E Fund Nikkei 225 ETF and Nikkei ETF rose as high as 10.04% and 8.22% respectively on May 19th, closing at 1.469 yuan and 1.396 yuan. This is mainly related to the limited QD limit of the fund, but the high subscription demand.

Fluctuation or intensification after a sharp rise

Since the beginning of this year, the sectors with the highest growth rates have been - commercial companies, machinery, electrical appliances, automobiles, metals, and building materials. However, some driving factors of the stock market are gradually weakening in the short term. After a surge of over 20%, institutions have also increased their vigilance and begun to be more selective in their allocation targets.

Recently, the Japanese stock market has been experiencing volatility. For example, on July 20th, the Nikkei 225 index fell by more than 1%, and several Nikkei ETFs that Chinese investors had bet on also experienced declines. The Nikkei 225 ETF of Huaxia Nomura fell for two consecutive days, with declines of 2.25% and 1.03% on July 20th and 21st, respectively.

UBS stated that although the valuation is not high, the valuation of Japanese stocks has been significantly restored. Meanwhile, recent weekly data shows that the net trading value of foreign investors has begun to slow down. In addition, the repurchase volume may decrease in the future. In addition, the depreciation of the yen was previously one of the factors driving the rise of Japanese stocks, but as US interest rates approach their peak, further depreciation of the yen is unlikely to occur.

In terms of macro environment, the risk of the Federal Reserve continuing to aggressively raise interest rates has dissipated. At present, the market expects a probability of interest rate hikes in July to be over 95%. However, the market seems to have downplayed this impact and instead expects that there may be around 6 cumulative 150BP interest rate cuts next year, which is reflected in asset prices. Recently, the US dollar index has seen a continuous decline, falling below the 100 mark, and US bond yields have also turned downward.

UBS suggests maintaining selectivity in the short term and diversifying investments into some underperforming value stocks this year, including banks and domestic market oriented industries, to capture potential structural changes in Japan. Focus on two potential catalytic factors in the medium term: sustainable inflation and wage growth, and corporate governance driving an increase in ROE.

Specifically, after experiencing a considerable period of deflation, expectations for inflation remain the same as during the Abenomics period. In the early stages of Abenomics, the stock prices of the worst performing industries rose by more than 30%. Especially large enterprises and those benefiting from the weakening yen performed better than the TOPIX index. However, the difference this time is that banks, real estate, and small cap stocks did not perform well. This is because wage growth and inflation are currently high, so it is unlikely to be sustainable. Due to sustained inflation in Europe and America, while Japan's recovery cycle lags behind other countries, institutions believe that moderate inflationary pressure may continue to exist in the coming years.

"When investors are confident in Japan's moderate inflation dynamics and sustainable wage growth, these underperforming industries will outperform the benchmark index. In addition, if wage growth continues, domestic market oriented consumer free spending and service industries will also perform well," UBS analysts said.